“It was not the highly visible acts of Congress but the seemingly mundane and often nontransparent actions of regulatory agencies that empowered the great transformation of the U.S. commercial banks from traditionally conservative deposit-taking and lending businesses into providers of wholesale financial risk management and intermediation services.” — Professor Saule Omarova, “The Quiet Metamorphosis, How Derivatives Changed the Business of Banking” University of Miami Law Review, 2009

While the world is absorbed in the U.S. election drama, the derivatives time bomb continues to tick menacingly backstage. No one knows the actual size of the derivatives market, since a major portion of it is traded over-the-counter, hidden in off-balance-sheet special purpose vehicles. However, when Warren Buffet famously labeled derivatives “financial weapons of mass destruction” in 2002, its “notional value” was estimated at $56 trillion. Twenty years later, the Bank for International Settlements estimated that value at $610 trillion. And financial commentators have put it as high as $2.3 quadrillion or even $3.7 quadrillion, far exceeding global GDP, which was about $100 trillion in 2022. A quadrillion is 1,000 trillion.

Most of this casino is run through the same banks that hold our deposits for safekeeping. Derivatives are sold as “insurance” against risk, but they actually add a heavy layer of risk because the market is so interconnected that any failure can have a domino effect. Most of the banks involved are also designated “too big to fail,” which means we the people will be bailing them out if they do fail.

Derivatives are considered so risky that the Bankruptcy Act of 2005 and the Uniform Commercial Code grant them (along with repo trades) “super-priority” in bankruptcy. That means if a bank goes bankrupt, derivative and repo claims are settled first, drawing from the same pool of liquidity that holds our deposits. (See David Rogers Webb’s The Great Taking and my earlier articles here and here.) A derivatives crisis could easily vacuum up that pool, leaving nothing for us as depositors — or for the “secured” creditors who are junior to derivative and repo claimants in bankruptcy, including state and local governments.

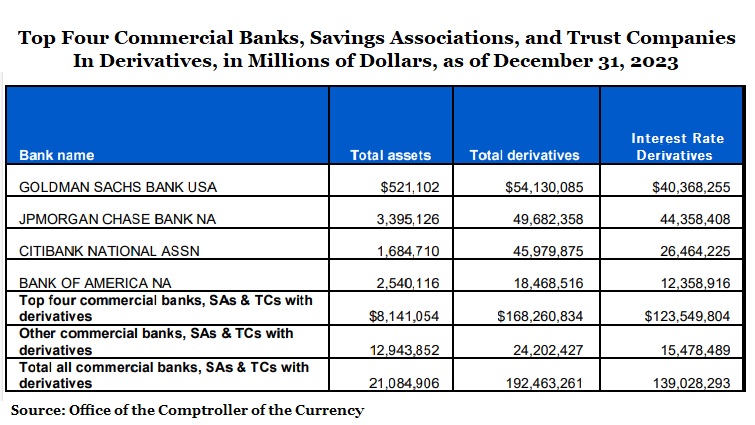

As detailed by Pam and Russ Martens, publisher and editor, respectively of Wall Street on Parade, as of Dec. 31, 2023, Goldman Sachs Bank USA, JPMorgan Chase Bank N.A., Citigroup’s Citibank and Bank of America held a total of $168.26 trillion in derivatives out of a total of $192.46 trillion at all U.S. banks, savings associations and trust companies. That’s four banks holding 87 percent of all derivatives at all 4,587 federally-insured institutions then in the U.S.

In June 2024, the Federal Deposit Insurance Corporation (FDIC) and the Federal Reserve Board jointly released their findings on the eight U.S. megabanks’ “living wills” – their resolution or wind-down plans in the event of bankruptcy. The Fed and FDIC faulted all of the four largest derivative banks on shortcomings in how they planned to wind down their derivatives.

How Banks Guarding Our Deposits Became the Biggest Gamblers in the Derivatives Casino

Banks are not just middlemen in the derivatives market. They are active players taking speculative positions. In this century, writes Professor Omarova, the largest U.S. commercial banks have emerged “as a new breed of financial super-intermediary—a wholesale dealer in financial risk, conducting a wide variety of capital markets and derivatives activities, trading physical commodities, and even marketing electricity.” She notes that the Federal Reserve has allowed several financial holding companies to purchase and sell physical commodities (including oil, natural gas, agricultural products and electricity) in the spot market to hedge their commodity derivative activities, and to take or make delivery of those commodities to settle the transactions.

It was not Congress that authorized that expansive definition of permitted banking activities. It was the Office of the Comptroller of the Currency (OCC), part of the “administrative deep state,” that permanent body of unelected regulators who carry on while politicians come and go. As Omarova explains:

Through seemingly routine and often nontransparent administrative actions, the OCC effectively enabled large U.S. commercial banks to transform themselves from the traditionally conservative deposit-taking and lending institutions, whose safety and soundness were guarded through statutory and regulatory restrictions on potentially risky activities, into a new breed of financial “super-intermediaries,” or wholesale dealers in pure financial risk. …

Moreover, some of the most influential of those decisions escaped public scrutiny because they were made in the subterranean world of administrative action invisible to the public, through agency interpretation and policy guidance.

The OCC’s authority to regulate banks dates back to the National Bank Act of 1863, which grants national banks general authority to engage in activities necessary to carry on the “business of banking,” including “such incidental powers as shall be necessary to carry on the business of banking.” The “business of banking” is not defined in the statute. Omarova writes:

Section 24 (Seventh) of the National Bank Act grants national banks the power to exercise all such incidental powers as shall be necessary to carry on the business of banking; by discounting and negotiating promissory notes, drafts, bills of exchange, and other evidences of debt; by receiving deposits; by buying and selling exchange, coin, and bullion; by loaning money on personal security; and by obtaining, issuing, and circulating notes.

No mention is made of derivatives trading or dealing.

The powers of banks were further limited by Congress in the Glass-Steagall Act of 1933, which explicitly prohibited banks from dealing in corporate equity securities, and by other statutes passed thereafter. However, the portion of the Glass-Steagall Act separating depository from investment banking was reversed in the Commodity Futures Modernization Act in 2000. Omarova writes that this allowed the OCC to articulate “an overly expansive definition of the ‘business of banking’ as financial intermediation and dealing in financial risk, in all of its forms, and … this pattern of analysis allowed the OCC to expand the range of bank-permissible activities virtually without any statutory constraint.”

What Then Can be Done?

The 2008 financial crisis is now acknowledged to have been largely a derivatives crisis. But massive efforts at financial reform in the following years have failed to fix the underlying problem. In a Forbes article titled “Big Banks and Derivatives: Why Another Financial Crisis Is Inevitable,” Steve Denning writes:

Banks today are bigger and more opaque than ever, and they continue to trade in derivatives in many of the same ways they did before the crash, but on a larger scale and with precisely the same unknown risks.

Most of this derivative trading is conducted through the biggest banks. A commonly held assumption is that the real derivative risk is much smaller than the “notional amount” stated on the banks’ balance sheets, but Denning observes:

[A]s we learned in 2008, it is possible to lose a large portion of the “notional amount” of a derivatives trade if the bet goes terribly wrong, particularly if the bet is linked to other bets, resulting in losses by other organizations occurring at the same time. The ripple effects can be massive and unpredictable.

In 2008, governments had enough resources to avert total calamity. Today’s cash-strapped governments are in no position to cope with another massive bailout.

He concludes:

Regulation and enforcement will only work if it is accompanied by a paradigm shift in the banking sector that changes the context in which banks operate and the way they are run, so that banks shift their goal from making money to adding value to stakeholders, particularly customers. This would require action from the legislature, the SEC, the stock market and the business schools, as well as of course the banks themselves.

A Paradigm Shift in “the Business of Banking”

In a September 2023 paper titled “Rebuilding Banking Law: Banks as Public Utilities,” Yale law professor Lev Menand and Vanderbilt law professor Morgan Ricks propose shifting the goal of banking so that chartered private banks are “not mere for-profit businesses; they have affirmative obligations to the public.” The authors observe that under the New Deal framework, which was rooted in the National Bank Act of 1864, banks were largely governed as public utilities. Charters were granted only where consistent with public convenience and need, and only chartered banks could expand the money supply by extending loans.

The Menand/Ricks proposal is quite detailed and includes much more than regulating derivatives, but on that specific issue they propose:

While member banks are permitted to enter into interest-rate swaps to hedge rate risk, they are not allowed to engage in derivatives dealing (intermediation or market making) or take directional bets in the derivatives markets. Derivatives dealing and speculation do not advance member banks’ monetary function. Apart from loan commitments, member banks would not be in the business of offering guarantees or other forms of insurance.

Would that mean the end of the derivatives casino? No – it would just be moved out of the banks charged with protecting our deposits:

The blueprint above says nothing about what activities can take place outside the member banking system. It says only that those activities can’t be financed with run-prone debt [meaning chiefly deposits]. In principle, we could imagine a very wide degree of latitude for non bank firms, subject of course to appropriate standards of disclosure, antifraud, and consumer and investor protection. So securities firms and other nonbanks might be given free rein to engage in structured finance, derivatives, proprietary trading, and so forth. But they would not be allowed to “fund short.”

By “funding short,” the authors mean basically “creating money,” for example through repo trades in which short-term loans are rolled over and over. In their proposal, only chartered banks are delegated the power to create money as loans.

Expanding the Model

University of Southampton business school professor Richard Werner, who has written extensively on this subject, adds that banks should be required to concentrate their lending on productive ventures that create new goods and services and avoid inflating existing assets such as housing and corporate stock.

Speculative derivatives are a form of “financialization” – money making money without producing anything. The winners just take money from the losers. Gambling is not illegal under federal law, but the chips in the casino should not be our deposits or loans made with the backing of our deposits.

The Menand/Ricks proposal is for private banks, but banks can also be made “public utilities” through direct ownership by the government. The stellar model is the Bank of North Dakota, which does not speculate in derivatives, cannot go bankrupt, makes productive loans, and has been highly successful. (See earlier article here.) The public utility model could also include a national infrastructure bank, as proposed in H.R. 4052, which currently has 37 co-sponsors.

The “business of banking” can include making money for private shareholders and executives, but that business should be junior to the public interest, which would prevail when they conflict.

Unfortunately, only Congress can change the language of the controlling statute; and Congress has been motivated historically to make major changes in the banking system only in response to a Great Depression or Great Recession that exposes the fatal flaws in the existing system. With the reversal of “Chevron deference,” however, the OCC’s rules can now be challenged in court. A powerful citizen’s movement might be able to catalyze needed changes before the next Great Depression strikes.

A financialized economy is not sustainable and not competitive. The emphasis should be on investment in the real economy. That is the sort of paradigm shift that is necessary if the U.S. is to survive and prosper.

*

Click the share button below to email/forward this article to your friends and colleagues. Follow us on Instagram and Twitter and subscribe to our Telegram Channel. Feel free to repost and share widely Global Research articles.

Spread the Truth, Refer a Friend to Global Research

This article was first posted as an original to ScheerPost.com.

Ellen Brown is an attorney, founder of the Public Banking Institute, and author of thirteen books including Web of Debt, The Public Bank Solution, and Banking on the People: Democratizing Money in the Digital Age. Her 400+ blog articles are posted at EllenBrown.com. She is a regular contributor to Global Research.

Featured image: © 2018 Advantus Media, Inc. and QuoteInspector.com