The Corona Pandemic and Trump’s Trade War against China: America’s Dependence on “Made in China”. Potential Disruption of the US Economy

In real economy terms, China is the largest national economy Worldwide, far surpassing the US

First published in May 2020, updated June 14, 2020

What Prospects for trade relations with China, in the wake of the 2020 US November Presidential Election?

Introduction

The US has been threatening China with trade sanctions for several years. At the outset of the Trump administration in January 2017, Washington not only envisaged punitive trade measures, it also called for “an investigation into China’s trade practices” focussing on alleged violations of U.S. intellectual property rights.

This initiative was then followed by renewed threats to “impose steep tariffs on Chinese imports [into the US], rescind licenses for Chinese companies to do business in the United States….” And then in September of 2019 “The Trump administration enacted tariffs on roughly $112 billion worth of Chinese imports,”

An understanding of the geopolitical and strategic dimensions is crucial. The conflict with China is not limited to bilateral trade. President Trump’s political rhetoric directed against China has become increasingly aggressive. Washington’s unspoken objective is to derail China’s Belt and Road Initiative (BRI) which consists in developing trade relations with a large number of partner countries in major regions of the World.

China’s Belt and Road Initiative (BRI) predicated on Eurasian economic integration is viewed by Washington as an encroachment on US hegemonic interests.

“Over time the BRI could threaten the very foundations of Washington’s post-WWII hegemony”,(Thomas P. Cavanna The Diplomat)

US hegemony is also coupled with US militarization of strategic waterways in the East and South China seas combined with numerous US military bases in locations within proximity of China.

In a bitter irony, the rhetorical gush of threats by president Donald Trump, was accompanied by seemingly “constructive” bilateral trade negotiations leading up to the signing of the First Phase of a detailed and comprehensive Economic and Trade Agreement between the United States and China in mid-January 2020 at the very outset of the coronavirus pandemic in China.

According to U .S. analysts this historic Agreement signed on January 15, 2020 would “hopefully signal the beginning of the end of the trade war“.

But that did not happen.

China-US Relations and The Corona Pandemic

Two weeks after the signing of the Agreement, the Trump administration announced the curtailment of air travel with China, which was accompanied by the disruption of transportation and trade relations with China, with repercussions on China’s export manufacturing sector.

Trump’s decision on January 31, 2020 was taken immediately following the announcement by the WHO Director General of a Public Health Emergency of International Concern (PHEIC) (January 30, 2020). In many regards, this was an act of “economic warfare” against China.

And then, following Trump’s January 31st decision to curtail air travel and transportation to China, a campaign was launched in Western countries against China as well against ethnic Chinese. The Economist reported that “The coronavirus spreads racism against and among ethnic Chinese”

“Britain’s Chinese community faces racism over coronavirus outbreak”

According to the South China Morning Post (Hong Kong):

“Chinese communities overseas are increasingly facing racist abuse and discrimination amid the coronavirus outbreak. Some ethnic Chinese people living in the UK say they experienced growing hostility because of the deadly virus that originated in China.”

And this phenomenon happened all over the U.S.

China Town, San Fransisco

US-China Trade. America’s Dependence on “Made in China”

The unspoken truth is that America is an import led economy with a weak industrial and manufacturing base, heavily dependent on imports from the PRC. Despite America’s financial dominance and the powers of the dollar, there are serious failures in the structure of America’s “Real Economy”: i.e marked by the closing down of factories as well as failures at the level of both physical and social infrastructure.

This Import-led economic structure has a long history. It was the result of US policies formulated in the late 1970s and early 1980s to delocate a large part of its industrial base to “low cost” locations in China including the Special Economic Zones (SEZ) (created in 1979) and the “development zones” or “special trading areas” (established in 14 designated coastal cities in 1984).

A large share of US manufacturing was relocated, followed by a later stage of relocation of several high technology production sectors.

High Technology

The US no longer has a hegemony in high technology production and intellectual property. In the course of the last decade, China has consolidated its position. China is now leading in several areas of high tech development and production which are dependent on Chinese owned intellectual property.

This inevitably had repercussions on California’s Silicone Valley, the once prosperous cradle of high tech industries and research labs.

A contradictory relationship has evolved in which the US is not only dependent on “Made in China” imported manufactured goods, China has surpassed the US in several areas of high technology including the telecom industry and 5G:

All the cases form a big picture in which Washington and its allies are suppressing Chinese telecom companies. Huawei is the world’s largest telecom equipment maker and second largest smartphone manufacturer in the world. It also produces high-quality chips. It is pathetic that such a comprehensive high-tech enterprise [Hwawei] is accused and undermined. The US is realizing its political purposes by judicial means. (Global Times, January 17, 2019)

According to the Wharton Business School (University of Pennsylvania, emphasis added):

“China’s technology sector has grown so rapidly in the last two decades that it is pushing the United States out of its long-held position at the top of the digital food chain. Advancements by companies like Huawei, WeChat, Baidu, Tencent and others are helping the Chinese economy grow at an unprecedented rate and influencing the global economy. China and the U.S. are battling to be the leader in 5G technology, a fight it seems that Chinese tech companies are winning.

According to author Rebecca Fanning “The U.S. needs a policy that can address China’s rise in technology”. It would appear that the “policy” contemplated by Washington precludes the notion of US “acceptance” of China’s lead in several high technology sectors.

“China has top-down government directives that are propelling the country forward in all kinds of technology sectors. The “Made in China 2025” [plan] has designated time periods where China is going to lead globally in certain sectors, and the U.S. really does not have anything that’s the equivalent to that.” (Wharton School Interview, emphasis added)

The “Made in China 2025” 中国制造2025 first launched by Beijing in May 2015, essentially consists in supporting the high technology sectors while also upgrading China’s industrial base in manufacturing. The Made in China 2025 agenda also “highlights green manufacturing, energy saving and new energy vehicles, high-end equipment manufacturing, including new information technology and robotics…” (Global Times, May 20, 2015)

Made in China: Retail Trade in the US

Imagine what would happen if president Trump decided from one day to the next to significantly curtail America’s “Made in China” imports. It would be absolutely devastating, disrupting the consumer economy, an economic and financial chaos.

A large share of goods displayed in America’s shopping malls, including major brands is “Made in China”.

A large share of goods displayed in America’s shopping malls, including major brands is “Made in China”.

“Made in China” also dominates the production of a wide range of industrial inputs, machinery, building materials, automotive, parts and accessories, etc. not to mention the extensive sub-contracting of Chinese companies on behalf of US conglomerates.

What the Trump Administration does not comprehend is how the US trade deficit ultimately benefits the US Economy. It contributes to sustaining America’s retail economy, it also sustains the growth of America’s GDP.

“Made in China” is the backbone of retail trade which indelibly sustains household consumption in virtually all major commodity categories from clothing, footwear, hardware, electronics, toys, jewellery, household fixtures, food, TV sets, mobile phones, etc.

Ask the American consumer: The list is long. “China makes 7 out of every 10 cellphones sold Worldwide, as well as 12 and a half billion pairs of shoes’ (more than 60 percent of total World production). Moreover, China produces over 90% of the World’s computers and 45 percent of shipbuilding capacity (The Atlantic, August 2013) .

It is the source of tremendous profit and wealth in the US. Consumer commodities imported from China’s low cost economy are often sold at the retail level ten times their factory price. This process creates a “value added” which then leads to an increase in Gross Domestic Product.

In a wide range of economic activities, production does not take place in the USA. The producers have given up production.

The US trade deficit with China is instrumental in fuelling the profit driven consumer economy which relies on Made in China consumer goods.

Case studies suggest that China imports trigger an increase in value added in the US of 8-10 times the factory price of the commodities imported from China. What this means is that a large share of US GDP growth is attributable to production outside the US, namely China. Without Chinese imports, the US growth of GDP would inevitably be undermined.

What this signifies is that in real economy terms, China is the largest national economy Worldwide.

Chinese policy makers are fully aware that the US economy is heavily dependent on “Made in China”.

Trump: The “Paper Tiger”. How does the Coronavirus Crisis affect US-China Relations?

Trump: The “Paper Tiger”. How does the Coronavirus Crisis affect US-China Relations?

With an internal market of more than 1.4 billion people, coupled with The Belt and Road initative and a buoyant global export market, the veiled threats by President Trump are not always taken seriously. Trump is “A Paper Tiger”. In the words of Mao Zedong:

“Now U.S. imperialism is quite powerful, but in reality … it is nothing to be afraid of, it is a paper tiger. Outwardly a tiger, it is made of paper, unable to withstand the wind and the rain… (US Imperialism is a Paper Tiger, Selected Works, 1951)

Bilateral Trade Crisis

US imports from China have declined significantly as a result of the pandemic, the impacts on US retail trade are potentially devastating. In this review, we should distinguish between the following factors:

1) The disruption in trade largely triggered by concrete economic factors (production, supply lines, international transport caused by the corona crisis. This process of disruption was largely initiated in late January early February).

2) The disruption of a political and geopolitical nature largely related to accusations and threats by the Trump administration, claiming that China is responsible for “spreading the virus”. These accusations started in April. At the time of writing, there is no evidence that president Trump’s accusations have a bearing on the April commodity trade figures analyzed below. In April the tendency was towards a recovery of US-China trade.

Disruption in US-China Commodity Trade

It is difficult to assess the implications of the most recent wave of Trump accusations. Despite Trump’s most recent threats, the January 15th, 2020 bilateral US-China trade agreement has been signed.

2018-2019 Data

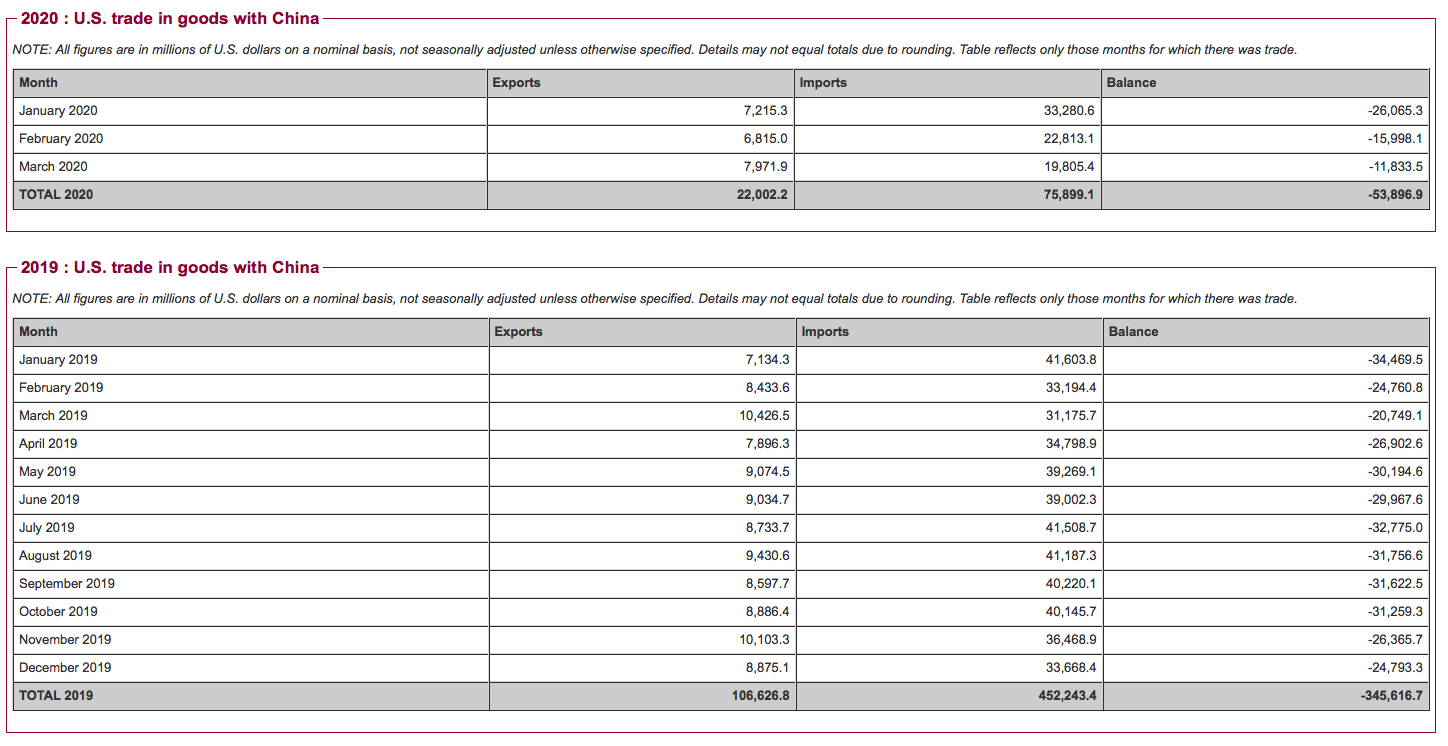

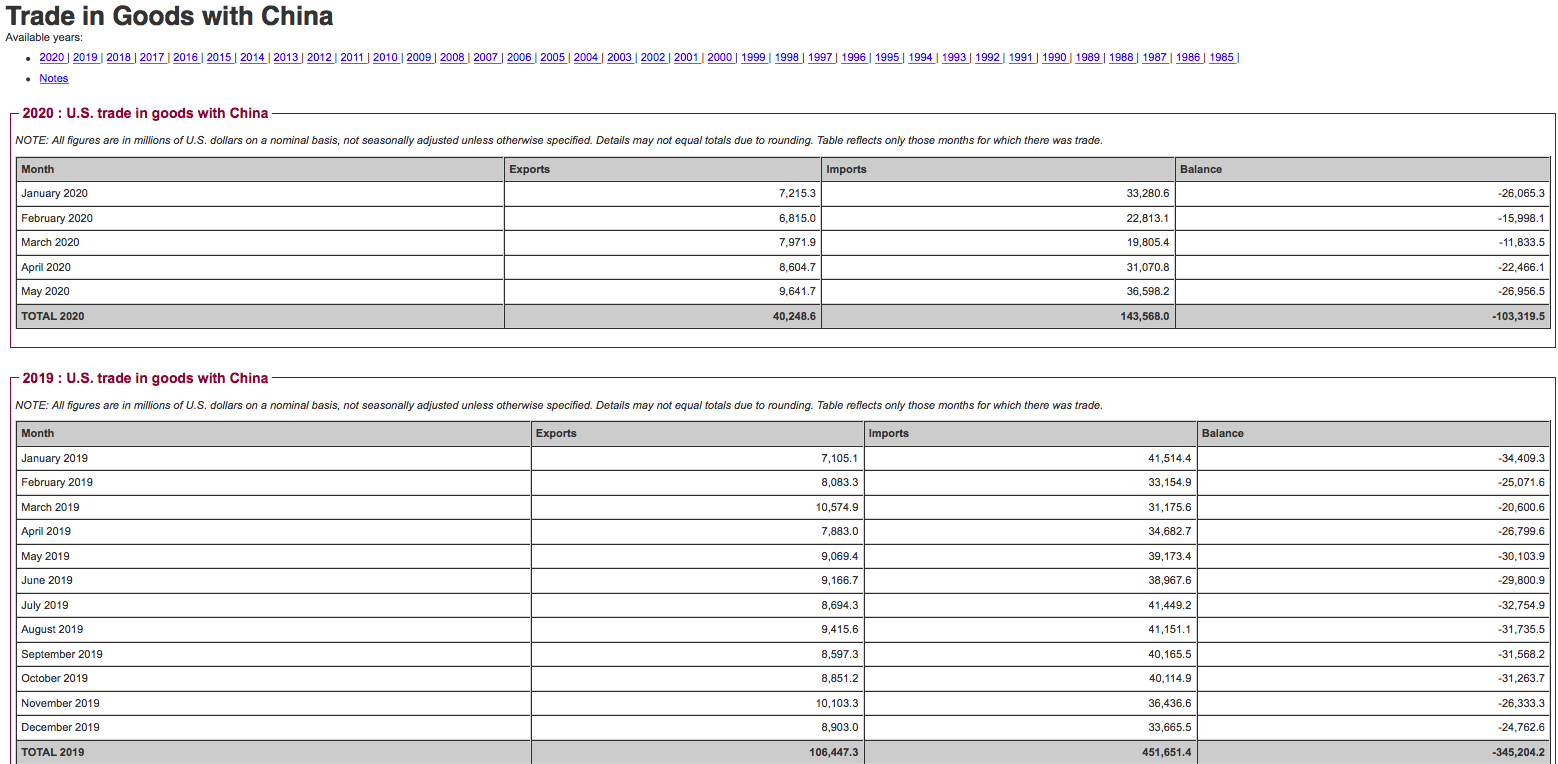

US imports from China were of the order of $452.243 billion. In contrast, US exports from the US to China were of the order of $106.627 billion reflecting a significant decline in bilateral US-China trade in relation to 2018.

The US trade deficit with China in 2019 was a staggering $345.617 billion.

January-April 2020

The available monthly figures for 2020 suggest a substantial decline in (monthly) US commodity imports from China (in relation to 2019): A 28.3% decline (average over first three months of 2o2o in relation to first 3 months of 2019), largely attributable to the coronavirus crisis.

What are the prospects? The decline of US imports from China in the month of March was of a staggering 36.5% in relation to March 2019.

Does this figure indicate a significant collapse in US-China trade?

While China’s export economy is in the process of normalization in the wake of the China pandemic, the political confrontations including the accusations directed against China by president Trump could potentially lead to a “slump” in US-China bilateral trade.

Moreover, according to figures quoted by the the Financial Times (largely attributable to the deep-seated financial crisis which started in February 2020), the value of newly announced Chinese direct investment projects into the US has fallen by about 90%: $200m in the first quarter of 2020, down from an average of $2bn per quarter in 2019.

“Chinese direct investment into the US stood at $5bn, a slight drop from $5.4bn in 2018 and well off a recent peak of $45bn in 2016, when Chinese companies were much more free to acquire US counterparts”

What is significant, however, is that China’s overall exports (dollars) in April rose by 3.5% (in relation to April 2019), according to data from China’s General Administration of Customs released in early May. While these figures reflect a recovery of China’s overall export trade, China’s exports to the US in April experienced a significant decline, namely 7.9%. Similarly, in May there was decline of 8.5% in relation to May 2019.

A major redirection of China’s exports has taken place:

A 3.5 % overall increase in exports coupled with a 7.9% decline in exports to the US, which inevitably will have a detrimental impact on the U.S. economy.

Exports to the US in April were of the order of the order of 32,060.4 million (compared to 34,798.9 million in April 2019). In contrast, compensating for the decline in exports to the US, China’s Eurasian trade has picked up.

China’s total imports in April 2020 fell 14.2% in relation to the same period in 2019. China’s trade surplus for the month of April was a staggering $45.34 billion.

China Viewed as a “Threat” by the Trump Whitehouse.

How will US-China Relations evolve?

The US president is not only blaming China for the corona pandemic without a shred of evidence, his newly appointed Director of National Intelligence (DNI) Rep. John Ratcliffe stated unequivocally at the US Senate confirmation hearing:

“I view China as the greatest threat actor right now,”

“Look with respect to COVID-19 and the role China plays; the race to 5G; cybersecurity issues: all roads lead to China,” he told the panel. (emphasis added)

To which the Senate Committee asked him to clarify:

“whether he would politicize the intelligence process to keep the president happy”.

Does this appointment have a bearing on the future of US-China relations?

On May 21, Rep Ratcliffe was nominated as Director of National Intelligence (DNI) with a mandate to “counter threats from great powers” on behalf of the Trump Whitehouse.

The Director of the DNI oversees and coordinates 16 intelligence bodies, including the CIA, the National Security Agency (NSA), and the FBI’s counterintelligence division.

The head of the DNI has links to the White House. While the DNI coordinates the various Intel entities, it is not intelligence agency. Declarations from the head of the DNI are more of political nature. Will Ratcliffe’s declarations be used in support of Trump’s 2020 election campaign?

UPDATE ON US-CHINA TRADE (includes figures for May 2020, reflects a decline of 8.5% in relation to May 2019).

***

Michel Chossudovsky is an award-winning author, Professor of Economics (emeritus) at the University of Ottawa, Founder and Director of the Centre for Research on Globalization (CRG), Montreal, Editor of Global Research. He has taught as visiting professor in Western Europe, Southeast Asia, the Pacific and Latin America. He has served as economic adviser to governments of developing countries and has acted as a consultant for several international organizations. He is the author of eleven books including The Globalization of Poverty and The New World Order (2003), America’s “War on Terrorism” (2005), The Global Economic Crisis, The Great Depression of the Twenty-first Century (2009) (Editor), Towards a World War III Scenario: The Dangers of Nuclear War (2011), The Globalization of War, America’s Long War against Humanity (2015). He is a contributor to the Encyclopaedia Britannica. His writings have been published in more than twenty languages.