There will be no more taxpayer bailouts for the Big Wall Street banks. That much has been established by the lobbied to death Dodd-Frank banking reform (yeah, right) bill.

However, instead of taking money from the government (taxpayers), the principal has been established that the next source of money for profligate banks will be your deposit accounts. Yeah, that’s right, the money to stabilize the banking sector during the next crisis will come out of your savings and checking accounts.

To add insult to injury – since the banks pay you zero percent on your savings account in the first place – the banks have the right to confiscate your funds if they crash the economy again as they did in 2008. Remember the Great Recession? It’s coming again to a bank near you.

How can they do this, you ask?

Simple. When you deposit money in a checking or savings account, that money no longer belongs to you. Technically and legally, it becomes the property of the bank, and the bank just issues you what amounts to an IOU. As far as the bank is concerned, it’s an unsecured debt.

The way Dodd-Frank has managed to screw things around, derivatives (bets banks have made in the Wall Street casino) have priority over your checking and savings accounts when it comes to paying off their debts. And don’t think that the FDIC (Federal Deposit Insurance Corporation) will save your money. The assets of the FDIC are minuscule (in the billions) compared to the valuation of outstanding derivatives (in the trillions). Your deposits are protected only up to the $250,000 insurance limit, and also only to the extent that the FDIC has the money to cover deposit claims or can come up with it.

Ellen Brown asks, “What happens when Bank of America or JPMorganChase, which have commingled their massive derivatives casinos with their depositary arms, is propelled into bankruptcy by a major derivatives fiasco? These two banks both have deposits exceeding $1 trillion, and they both have derivatives books with notional values exceeding the GDP of the world.”

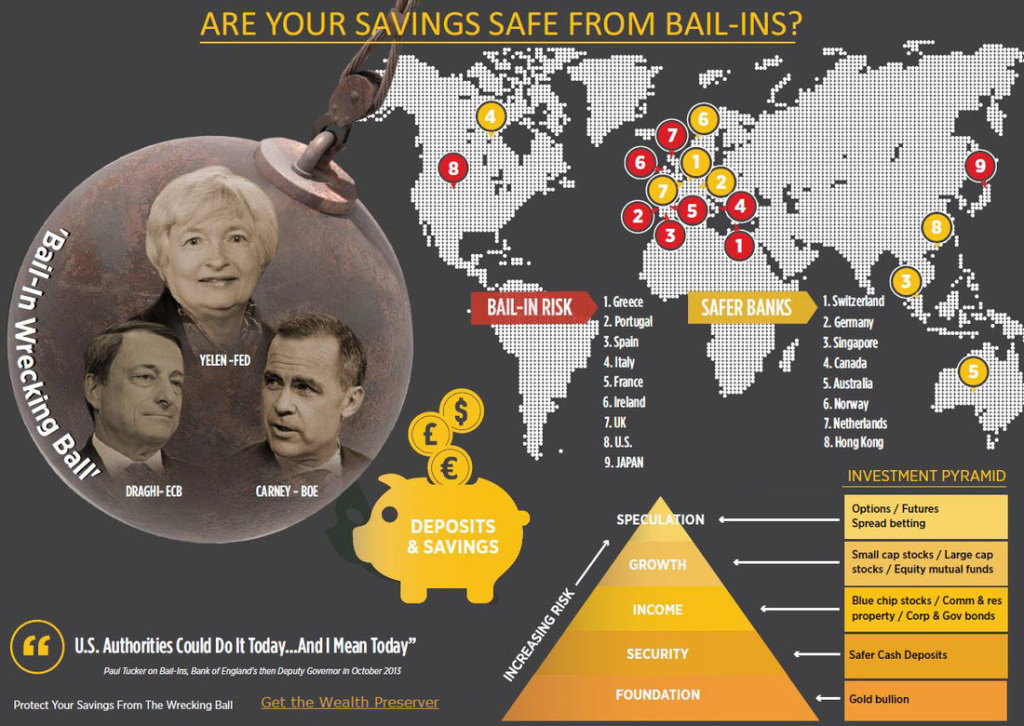

The answer is a Cypress style bail-in.

You might recall that money was taken out of depositor’s accounts during the last banking crisis in Cypress. These depositors were mainly Russian oligarchs so what the heck. Now this principle has been extended to depositors in the big Wall Street banks and actually to depositors all over the world. Now is a good time to take your money out of banks such as Bank of America, JPMorgan Chase and Citibank and deposit it in smaller banks or credit unions. Otherwise, $1 trillion of depositors’ funds could go bye-bye, and that’s not small change.

You might recall that money was taken out of depositor’s accounts during the last banking crisis in Cypress. These depositors were mainly Russian oligarchs so what the heck. Now this principle has been extended to depositors in the big Wall Street banks and actually to depositors all over the world. Now is a good time to take your money out of banks such as Bank of America, JPMorgan Chase and Citibank and deposit it in smaller banks or credit unions. Otherwise, $1 trillion of depositors’ funds could go bye-bye, and that’s not small change.

Ellen Brown elucidates:

According to an International Monetary Fund paper titled “From Bail-out to Bail-in: Mandatory Debt Restructuring of Systemic Financial Institutions”:

[B]ail-in . . . is a statutory power of a resolution authority (as opposed to contractual arrangements, such as contingent capital requirements) to restructure the liabilities of a distressed financial institution by writing down its unsecured debt and/or converting it to equity. The statutory bail-in power is intended to achieve a prompt recapitalization and restructuring of the distressed institution.

The language is a bit obscure, but here are some points to note:

- What was formerly called a “bankruptcy” is now a “resolution proceeding.” The bank’s insolvency is “resolved” by the neat trick of turning its liabilities into capital. Insolvent TBTF banks are to be “promptly recapitalized” with their “unsecured debt” so that they can go on with business as usual.

- “Unsecured debt” includes deposits, the largest class of unsecured debt of any bank. The insolvent bank is to be made solvent by turning our money into their equity – bank stock that could become worthless on the market or be tied up for years in resolution proceedings.

- The power is statutory. Cyprus-style confiscations are to become the law.

- Rather than having their assets sold off and closing their doors, as happens to lesser bankrupt businesses in a capitalist economy, “zombie” banks are to be kept alive and open for business at all costs – and the costs are again to be borne by us.

So as far as you, the depositor, are concerned, your money in checking and savings accounts is the bank’s “unsecured debt.” You will have to stand in line behind trillions of dollars of derivative payouts before your checking and savings accounts will be made whole. Both the Bankruptcy Reform Act of 2005 and the Dodd Frank Act provide special protections for derivative counterparties, giving them the legal right to demand collateral to cover losses in the event of insolvency.

They get first dibs, even before the secured deposits of state and local governments. Your chances of recovering your money are about as great as the chances of a snowball in hell.

Since most poor and middle class people have a major portion of their assets in checking and savings accounts while rich people have the major portion in real estate, stocks and bonds, who do you think will be most affected by bail-ins?

You guessed it: the poor and middle class will be hit the hardest. And don’t think your money will be safe in a bank’s safe deposit box. The banks have the right to go into your safe deposit box and take your money out of it.

Pension funds, which were the biggest suckers for Wall Street during the last banking crisis, will also be drained by Wall Street during the next one. Their funds will be subject to confiscation as bail-ins as well since many of the bonds they purchase are subject to being converted to bail-inable deposits if the banks really need the money which they no doubt will sooner or later when the derivatives bubble goes bust.

Pension funds, which were the biggest suckers for Wall Street during the last banking crisis, will also be drained by Wall Street during the next one. Their funds will be subject to confiscation as bail-ins as well since many of the bonds they purchase are subject to being converted to bail-inable deposits if the banks really need the money which they no doubt will sooner or later when the derivatives bubble goes bust.

So taxpayers you can sleep soundly as taxpayer bail-outs have been taken off the table in the next banking crisis. Whew, that’s a relief.

But if your savings get taken over by the bank, ouch, that’ll hurt even more than a widely distributed taxpayer bail-out which might add a couple of dollars to your income tax. Be careful of what you wish for. It could be even worse than what you already had.

There is a better way. Let the zombie banks go bankrupt instead of confiscating depositor funds. A better way is to create public banks and transfer funds from Wall Street. Then the gambling casino with all the attendant risks for bail-outs and bail-ins comes to an abrupt halt. Profits go to the local community or to the state in the case of North Dakota, the nations’s first and oldest public bank..

![]() On a personal note, a representative of my bank, Union Bank, called me a few weeks ago to inform me that I was only allowed five debits per month out of my savings account and that I had used up my five debits for December.

On a personal note, a representative of my bank, Union Bank, called me a few weeks ago to inform me that I was only allowed five debits per month out of my savings account and that I had used up my five debits for December.

So I would have to wait until January before I was allowed to take any more money out of my savings account. I was furious. “It’s my money isn’t it, and besides you call it a savings account. It gets zero interest.” He kept repeating that I was only allowed five debits per month and said it was a Federal law.

Well, this means nothing because it’s well known that all Federal banking regulations are written by lobbyists for the banking industry in the interests of the banking industry. I asked him what was the rationale for this regulation. He said, “The government doesn’t want you to spend your money too fast.” Hmmm. Since when does Big Brother have an interest in making sure I don’t spend my money? I don’t think so.

It probably has more to do with keeping your money in the bank so that the bank can meet its currency reserve requirements or possibly slow down the exodus of money from worthless savings accounts which pay no interest or even perhaps to confiscate your money for bail-ins during the next banking crisis at which time there will be undoubtedly a run on the banks 1930s style.

Whoops, if you’ve already had your five debits, you won’t be able to get your hands on your money before it’s “bailed-in.”

John Lawrence graduated from Georgia Tech, Stanford and University of California at San Diego. While at UCSD, he was one of the original writer/workers on the San Diego Free Press in the late 1960s. He founded the San Diego Jazz Society in 1984 which had grants from the San Diego Commission for Arts and Culture and presented both local and nationally known jazz artists. His website is Social Choice and Beyond which exemplifies his interest in Economic Democracy. His book is East West Synthesis. He also blogs at Will Blog For Food. He can be reached at [email protected].