“Last year, the corporations in the Russell 3000, a broad U.S. stock index, repurchased $567.6 billion worth of their own shares—a 21% increase over 2012, calculates Rob Leiphart, an analyst at Birinyi Associates, a research firm in Westport, Conn. That brings total buybacks since the beginning of 2005 to $4.21 trillion—or nearly one-fifth of the total value of all U.S. stocks today.” (Will Stock Buybacks Bite Back?, Wall Street Journal)

“$4.21 trillion” is a heckuva lot of froth. It means that the market is overpriced by at least 20 percent. Corporate bosses have been aggressively pumping up prices to reward shareholders even though earnings and revenues are looking increasingly shaky. The reason buybacks have caught fire is because– up to now– they’ve been considered a reasonably safe bet. With interest rates locked at zero, and the Central Bank flooding the financial system with $55 billion every month, stocks have been following the path of least resistance which is up, up, and away. (As of Friday, the S and P was up 176 percent from its March 2009 lows.)The point is, stock buybacks are a natural reaction to the Fed’s easy money policies. Corporations are just following the Fed’s lead. If the Fed didn’t want companies to engage in this kind of reckless behavior, it could either turn off the liquidity or raise rates. Either way, the buybacks would stop. The fact that the Fed keeps juicing the system just shows that the it’s real objective is to buoy stock prices regardless of the risks involved. And there are risks too. Keep in mind, that most of the money corporations use for buybacks is borrowed, which leaves them vulnerable to fluctuations in prices. If the market suddenly goes South, then over extended investors have to sell other assets to cover their bets. That leads to firesales, plunging prices and deflation.Surging margin debt is another sign of froth. Margin debt is money that investors borrow to finance the purchase of stocks. Margin debt has been trending higher since the recession ended in 2009, but it’s really skyrocketed in the last year as eager investors have piled into equities confident that the Fed has their back. The problem is that large amounts of margin debt usually indicate a peak in the market. Here’s a little background from an article in USA Today:

“The amount of money investors borrowed from Wall Street brokers to buy stocks rose for a seventh straight month in January to a record $451.3 billion, a potential warning sign that in the past has coincided with irrational exuberance and stock market tops…“One characteristic of getting closer to a market top is a major expansion in margin debt,” says Gary Kaltbaum, president of Kaltbaum Capital Management. “Expanding market debt fuels the bull market and is an investors’ best friend when stocks are rising. The problem is when the market turns (lower), it is the market’s worst enemy.”…“Forced liquidations can occur,” says Price Headley, CEO of BigTrends.com. “If the decline in the market is dramatic, it can cause a true flush-out, when everyone is getting forced out by margin calls.” (Record margin debt poses risk for bull market, USA Today)

Investors seem to think that the Fed has superhuman powers and can stop the market from correcting. But that’s a bad bet. Stocks will tumble, and when they do these same speculators will get a call from their broker telling them they need more cash to meet the required minimum. That “margin call” will lead to the dumping of stocks and other assets in a mad scramble for cash. If the margin call is broad-based enough, then debt deflation dynamics will kick in pushing down prices across the board paving the way for another spectacular stock market crash. That’s what happened in 2008 when a run on the shadow banking system (repo) sparked a panic that sent global shares plunging. Here’s a chartthat shows how closely stock prices follow the build up of margin debt.Like stock buybacks, margin debt is a natural reaction to Fed policy. Zero rates provide a subsidy for speculation while QE reduces the aggregate supply of financial assets thus pushing up prices. This is why there’s so much froth in the markets, because the Fed creates incentives for risk taking. Remove the incentives, and the bubbles quickly vanish. Poof.There are other areas where bubbles are emerging too, but it may be more worthwhile to consider “valuation metrics” which give us a better idea of where stock prices would be without the Fed’s liquidity injections. Here’s a brief excerpt from a post by John Hussman who’s done extensive research on the topic and who believes that the S&P 500 is currently more over-valued than the housing market in 2006:

“Based on valuation metrics that have demonstrated a near-90% correlation with subsequent 10-year S&P 500 total returns, not only historically but also in recent decades, we estimate that U.S. equities are more than 100% above the level that would be associated with historically normal future returns…It is the series of extreme instances over the past year that give investors the hope and delusion that historically reckless market conditions will lead only to further gains and greater highs. This is a mistake born of complacency in the face of a nearly uninterrupted, Fed-enabled 5-year market advance, and is the same mistake that was made in 2000 and again in 2007. By the time the present market cycle is completed, we expect the S&P 500 to be at least 40% lower than present levels.” (Hussman Warns S&P 500 Over-Valuation Now Higher Than Housing In 2006, Zero Hedge)

Okay, so what does that mean in plain English?It means that stocks are ridiculously overpriced, and the reason they’re overpriced is because the Fed has been juicing the market with easy money and monthly liquidity injections. Chief US Equity Strategist for Goldman Sachs, David J. Kostin, was even more blunt than Hussman. He said, “The current valuation of the S&P 500 is lofty by almost any measure, both for the aggregate market as well as the median stock.”So by any measure, the market is overvalued. That means that investors can expect either lower returns in the future or big losses. It’s going to be one or the other.So what are the chances that stocks will fall sharply in the next few months putting another dent in the pensions and life savings of the many of the Mom and Pop investors who just got back into the market in the last 12 months?I don’t have the foggiest idea. But the outlook is pretty bleak. Take a look at this from Mark Hulbert at Marketwatch:

“Nejat Seyhun, a finance professor at the University of Michigan, has found from his research…that only some (corporate) insiders have a consistently accurate view of their companies’ prospects.The insiders worth paying attention to are a company’s officers and directors…Prof. Seyhun — who is one of the leading experts on interpreting the behavior of corporate insiders — has found that … insiders do have impressive forecasting abilities. In the summer of 2007, for example, his adjusted insider sell-to-buy ratio was more bearish than at any time since 1990, which is how far back his analyses extended.Ominously, that degree of bearish sentiment is where the insider ratio stands today, Prof. Seyhun said in an interview.” (Corporate insider bearishness at pre-2008 crash levels; Opinion: Don’t ignore the behavior of executives in the know, Mark Hulbert, Marketwatch)

Then there’s this brief summary from Baupost Group founder and billionaire Seth Klarman who advises his clients to be prepared for a “trend reversal”. Here’s the quote from Business Insider:

“Six years ago, many investors were way out over their skis. Giant financial institutions were brought to their knees…The survivors pledged to themselves that they would forever be more careful, less greedy, less short-term oriented.But here we are again, mired in a euphoric environment in which some securities have risen in price beyond all reason, where leverage is returning to rainy markets and asset classes, and where caution seems radical and risk-taking the prudent course. Not surprisingly, lessons learned in 2008 were only learned temporarily. These are the inevitable cycles of greed and fear, of peaks and troughs.Can we say when it will end? No. Can we say that it will end? Yes. And when it ends and the trend reverses, here is what we can say for sure. Few will be ready. Few will be prepared.” (If You’re Bullish About Stocks, You Should Ponder This Warning From One Of The Smartest Investors Ever, Business Insider)

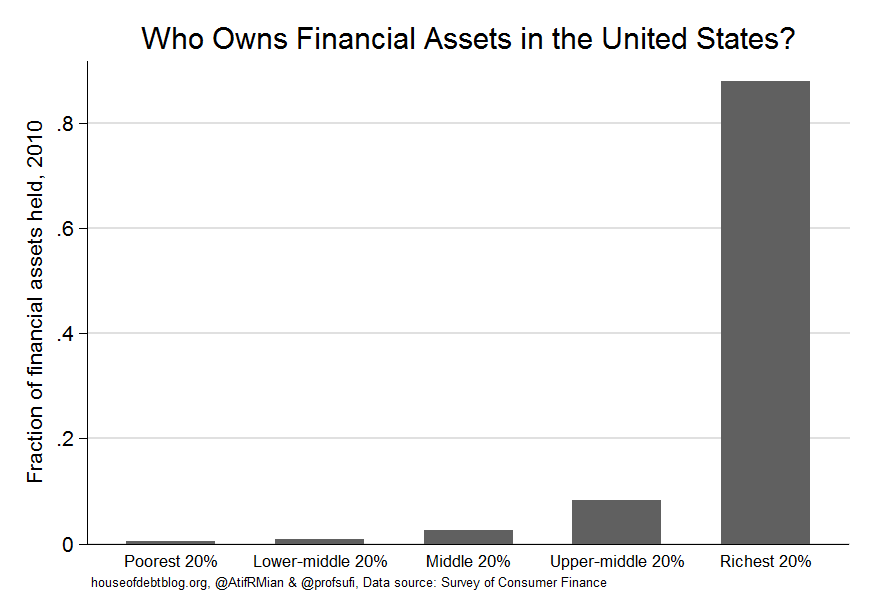

So the Fed has done what the Fed always does; set us up for another crash. Stocks are over-priced, insiders are selling and QE is winding down. It’s only a matter of time before the roof caves in and all hell breaks loose.But why? Why does the Fed keep steering the economy from one financial catastrophe to the next?That’s easy. Just take a look at this chart by economists Atif Mian and Amir Sufi and you’ll see for yourself who’s getting rich on this deal. This is the class of people who actually benefit from the Fed’s serial bubblemaking. Take a look:

“Here is the distribution of financial asset holdings across the wealth distribution. This is from the 2010 Survey of Consumer Finances:

The top 20% of the wealth distribution holds over 85% of the financial assets in the economy. So it is clear that the direct income from capital goes to the wealthiest American households.” (Capital Ownership and Inequality, House of Debt)

Who benefits from QE?Now you know.

MIKE WHITNEY lives in Washington state. He is a contributor to Hopeless: Barack Obama and the Politics of Illusion (AK Press). Hopeless is also available in a Kindle edition. He can be reached at [email protected].