The financial crisis of the past four years has thrown American families back two decades, according to figures provided by the Federal Reserve Board in its triennial Survey of Consumer Finances.

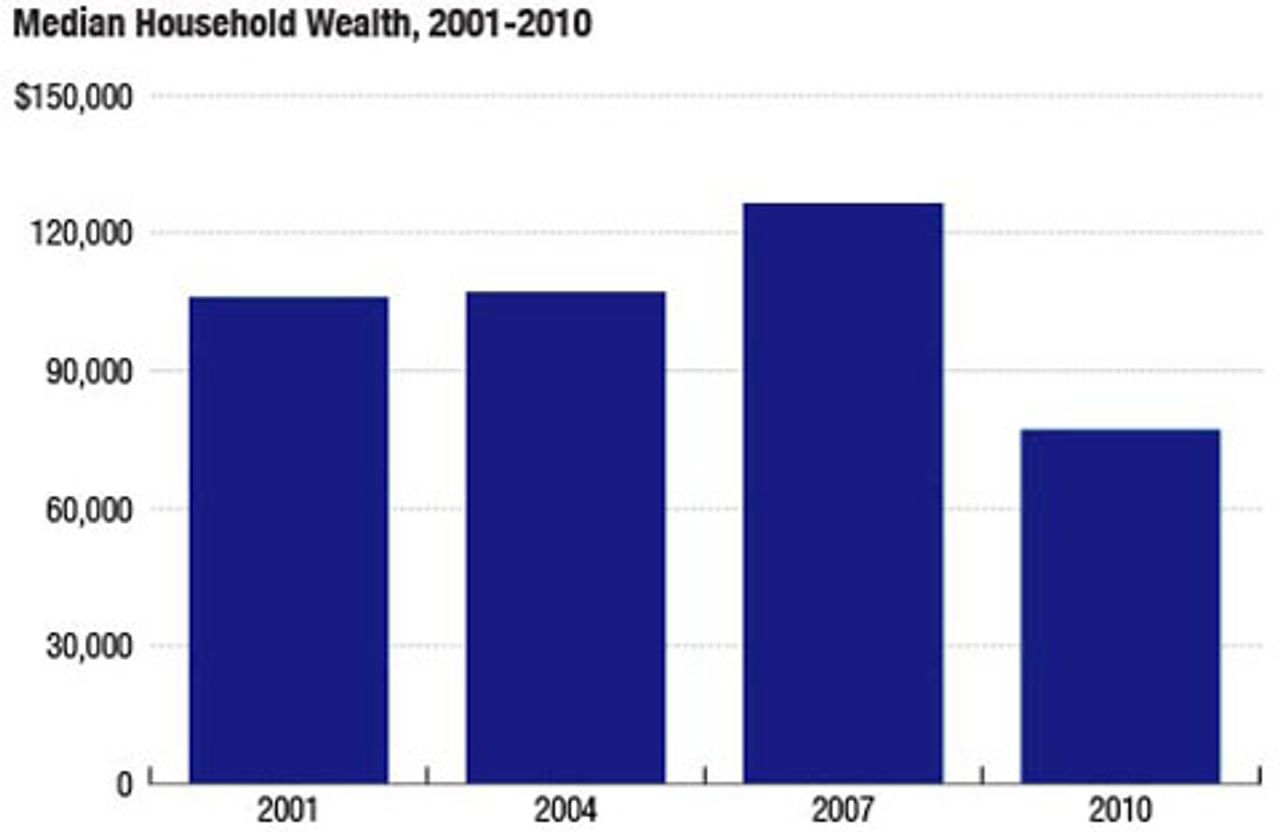

The median net worth of US families—the combined value of homes, bank accounts and other assets, minus mortgages and other debts—fell 38.9 percent between 2007 and 2010, from $126,400 to $77,300, approximately the level recorded in 1992. Median income also fell over the three-year period, down 7.7 percent before taxes, adjusting for inflation.

Source: Federal Reserve

Source: Federal Reserve

Credit: Lam Thuy Vo

The survey, based on interviews conducted in 2010 and early 2011, understates the impact of the ongoing economic slump, which has continued since then. Its figures on the distribution of wealth and income lag behind even more, since there has been a substantial rebound in the position of the wealthiest US households because of soaring corporate profits and rising stock prices.

Nonetheless, the clinically written 80-page document released Monday paints a devastating picture of the impact of four years of financial crisis and economic slump on working class families.

Some of the findings are like the tips of so many icebergs: they give only the barest glimpse of the profound suffering and exploitation experienced by tens of millions of people struggling to survive:

- Nearly two-thirds of all young families—those headed by someone under 35—owed installment payments on education debt, up from 53 percent in 2007.

- The proportion of families making use of so-called payday loans rose from 2.4 percent in 2007 to 3.9 percent in 2010, an increase of 65 percent.

- More than 10 percent of families with a 401(k) or other retirement account in 2007 had been compelled to liquidate it by 2010.

- The value of small businesses fell by an average of 20.5 percent from 2007 to 2010, with the steepest fall in the West and Northeast.

- Families headed by someone 75 or older sharply increased their use of credit card borrowing and carried larger balances.

- The proportion of families that reported they had been able to save any money during the previous year fell from 56.4 percent in 2007 to 52 percent in 2010.

Each one of these data points deserves exploration. In each case, investigation would illuminate an area of American social life ignored by the media and the candidates of the corporate-controlled Democratic and Republican parties.

The headline number of the Fed report, and deservedly so, is the dramatic fall in median net worth. This is the byproduct of the housing collapse, which has devastated the principal asset of working class and middle class families.

The median value of a US home fell by 42 percent between 2007 and 2010, from $95,300 to $55,000. At the same time, the burden of mortgage debt actually rose, from 51.3 percent of median home value to 64.6 percent, and 11.6 percent of homeowners with mortgages were under water, owing more on their homes than their present value.

In terms of income groups, the bottom 25 percent of households experienced a decline of 100 percent in median net worth, from a miniscule $1,300 per household in 2007 to zero in 2010. The second and third quartiles of the population saw decreases of 40 to 50 percent, while median net worth for the top 10 percent fell by only 6.4 percent (and has risen considerably since the end of 2010).

In other demographics, the biggest drops came in the West, the focal point of the housing collapse, where median net worth plunged 55.3 percent; for families headed by someone 35 to 44 years old, (down 54.4 percent); and for workers in white collar technical, sales or service occupations (down 57.7 percent).

The report details the enormous efforts by working people to survive financially by making sacrifices and cutting back on expenditures. Fewer families are carrying credit cards, the proportion carrying a balance dropped from 46.1 percent to 39.4 percent, and the median balance on those cards fell 16 percent from 2007 to 2010. Despite ever-greater repayments, however, debt as a percentage of family assets actually rose, from 14.8 percent to 16.4 percent, and the proportion of families behind on paying bills increased substantially.

In sum, these figures document a vast social retrogression, in which the financial position of the overwhelming majority of the American people is getting worse. This is not merely the result of impersonal economic processes, however. It is the direct consequence of decisions made in corporate boardrooms and in Washington that have exclusively benefited the super-rich at the expense of working people.

The Bush and Obama administrations and the Federal Reserve itself made countless trillions in public funds available to bail out the banks and billionaire investors, whose speculative manipulation drove the mortgage bubble and resulted in the greatest financial collapse since 1929. By comparison, only derisory sums were offered to hard-pressed homeowners faced with foreclosure, and not a penny has been allocated to directly create jobs for the tens of millions of unemployed.

The social crisis, which is today even deeper than in 2008, is a demonstration of two interconnected failures: the failure of capitalism as an economic system, and the failure of the two-party system, which is incapable of responding in any way to the growth of mass deprivation on a scale not seen since the 1930s.