All Global Research articles can be read in 51 languages by activating the Translate Website button below the author’s name.

To receive Global Research’s Daily Newsletter (selected articles), click here.

Click the share button above to email/forward this article to your friends and colleagues. Follow us on Instagram and Twitter and subscribe to our Telegram Channel. Feel free to repost and share widely Global Research articles.

***

At an over-excited anti-imperialist website, there is a fresh burst of hype about BRICS de-dollarisation. This is the second time since January that Ben Norton has made spectacular predictions about the end of US$ hegemony. And even at CounterPunch yesterday, two otherwise sensible commentators – Richard Wolff and Ramzy Baroud – chimed in with uncritical endorsement of the BRICS as a potential vehicle to undermine yankee-centric imperialist power.

Also, anytime there’s turbulence in global finance and the $ can be attacked, there will be a raft of personal-finance commentators who make money from investment churn, as well as pro-gold investment sites, and these hucksters really love the BRICS as a challenger – but more on them later. And Steve Forbes and Jim O’Neill have chimed in with a dash of cold water. Can’t trust any of them, but see the next email.

There are obvious temptations to headfall down this slippery slope. The geopolitical situation today appears new and different because of the alleged upscaling of multipolarity. But it’s not easy to translate these fast-shifting political and territorial alliances into monetary and currency strengths. Indeed what I’m reading now is all too reminiscent of 2014 just after the BRICS’ Fortaleza summit, when ‘alternatives’ to the IMF and World Bank were announced. At that point, a few others of my old friends also drank the BRICS kool-aid in their desperate thirst for alternative financial arrangements.

And we can always count on Pepe Escobar to be the most excited lad:

Russia and China are showing to the Global South that what American strategists had in store for them – you’re going to “freeze in the dark” if you deviate from what we say – is no longer applicable. Most of the Global South is now in open geoeconomic revolt… the most important vector is that both China and Russia, each exhibiting their own complex particularities – and both dismissed by the West as unassimilable Others – are heavily invested in building workable economic models that are not connected, in several degrees, to the Western financial casino and/or supply chain networks.

I should repeat that – in part because I worked inside the Fed on-and-off, in Washington and Philadelphia, from 1981-85, at the time the chair, Paul Volcker, was felling more Africans through economic violence than did Cecil Rhodes and King Leopold combined – you can count on me to be near the head of the queue seeking the end of US$ hegemony.

But in the just same skeptical way that Yanis Varoufakis posed the problem in Havana a few weeks ago, would we really expect anything fundamentally different, from the BRICS?

“Our New Non-Aligned Movement will fail if we give it a narrow role of bringing together the G77 and the BRICS in opposition to the West. We need to beware not only the functionaries in Washington or London or Brussels, who work tirelessly so that nothing changes, but also government officials in the pocket of capitalists in the Global South, including China, who use the US trade deficit to exploit their people, their country, and then stash their dollarised surplus value within the circuits of Wall Street and the City of London.”

Unfortunately, the article below by Norton draws off a brief, superficial interview Dilma Rousseff gave a few days ago to yet another bland, unthinking CGTN reporter. The line of argument unfolds in the tradition of overenthusiastic lefties who view the world as a series of nation-state conflicts – especially featuring the Rest against the West – instead of as diverse interstate, intrastate, class, social and political-ecological struggles in the context of overall capitalist crisis tendencies.

The best Dilma could offer was this generalisation:

We need a mechanism – a so-called anti-crisis mechanism – which must be counter-cyclical and support stabilization. At the same time it is necessary to find ways to avoid foreign exchange risk and other issues such as being dependent on the single currency such as the US dollar. The good news is that we are seeing many countries choosing to trade using their own currencies. China and Brazil for instance are agreeing to exchange with RMB in the Brazilian Real at the NDB we have committed to it in our strategy for the period from 2022 to 2026. NDB has to lend 30 % in local currency and so 30 % of our loan book will be financed in the currencies of our member countries. That would be extremely important to help our countries avoid exchange rate risks and shortage in finance that hinder long-term investments else here.

Not mentioned is that there is already such an anti-crisis mechanism, the BRICS Contingent Reserve Arrangement (CRA), which has not been used, and in any case it is ultimately just a way for the IMF to gain greater leverage since the CRA is tied to IMF ‘stabilisation’ packages which are pro-cyclical and ultimately destabilising.

As for the request for the NDB “to lend 30% in local currencies,” hang on, that means, firstly, 70% will be financed with Western currencies – typically the US$, which is extremely expensive unless the $ crashes, and yet with global financial instability underway it seems the $ is sticking to its relatively high post-2020 levels – and even the 30% in local currencies will not be provided in local interest rates, but instead be correlated to a rate consistent with expected devaluation (in relation to a basket of international currencies).

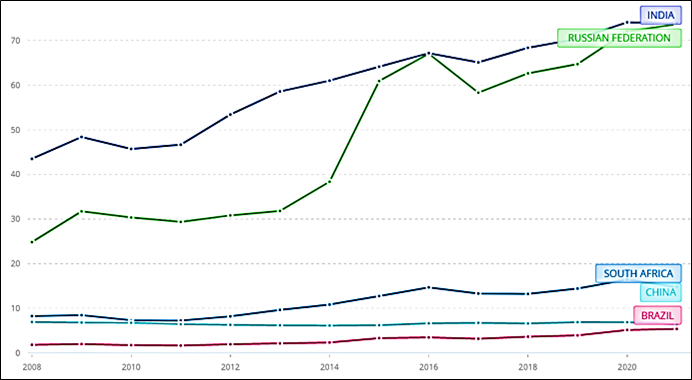

To maintain its international credit rating up, the BRICS NDB treasury would logically demand from borrowers much higher interest rates, in a period where we can expect four of the five BRICS to continue suffering currency depreciation. As the chart to the right shows, the Rupee went from 44/$ in 2008 to 75/$ in late 2021; and in the same period, the Ruble fell from 25/$ to 75/$; the Rand fell from 9/$ to 17/$; and the Real went from 2.2/$ to 5/$. Only the Renmimbi held steady.

As the blue area-graph below shows, the US$ was strongest in the 1980s, thanks to Volcker – and indeed had to be manipulated downwards by G7 finance ministers led by Baker and Brady in the U.S. And then it rose again during the 1998 Long Term Capital Management crash and the 2000-01 U.S. stock market dot.com collapse.

The collar bumped up again for the 2008 global financial meltdown. Then as the global commodity super-cycle ended in 2014-15 it spiked, as it did in 2020 with Covid lockdowns and in March 2022 with Putin’s Ukraine invasion.

The point is obvious: if there’s trouble in the world, even if it emanates from the U.S. as so many banking crises have, the $ gets a boost from investor flight to the supposedly safe $. Today, on an index basis that was 150 in 1985, the $ is still at 102, which is much higher than the average of the last 45 years, when it had dipped to as low as 72 on that index.

How about the sales of U.S. Treasury Bills by Beijing as an indicator? True, in January 2021, China owned $1.095 trillion of the total $28 trillion U.S. national debt – and last month the figure had dropped below $850 billion. But as was pointed out by Reuters, in reality China has been net buyers of $-denominated securities. The apparent decline in T-Bills was partly due to:

“valuation effects – recall that Treasuries had their worst year in decades last year – accounted for $114.4 billion, meaning the real decline in China’s holdings was ‘only’ $59.5 billion. This does not necessarily equate to outright selling. Some – probably most of it – was due to bonds maturing and not being reinvested. Meanwhile, China’s holdings of U.S. agency bonds last year rose by $50.9 billion and valuation effects accounted for $34.8 billion. This means the real increase was $85.9 billion, substantially more than the decline in Treasuries holdings. “Every holder of U.S. Treasuries in 2022 saw significant valuation losses. China’s losses are large but hardly unique,” said Brad Setser, an economist who is a senior fellow at the Council on Foreign Relations. “Maybe the big story is there is no sign that China’s dollar holding portfolio has changed much. There has been no significant shift since 2015-16.”

Back to the question of whether BRICS Bank loans should be in US$ or in local currency. This is a point made long ago by a prior BRICS Bank president from India, K.V. Kamath. Here’s how I wrote it up in 2016:

According to the SA foreign ministry’s Dave Malcolmson, there is strong political will to engage in non-dollar lending. Malcolmsen (2016) reported to Parliament about a 2015 presentation by KV Kamath, the NDB President. Amongst the innovative features of the NDB, “The actual challenge in respect of loan payments for developing countries pertain moreover to that of the currency fluctuation which increases the loan repayment terms (usually in USD) rather than agreed interest rates for such loans. He emphasized the importance of raising loans in local currencies to lessen such a burden.” Yet in its first five years, the vast majority of the $8 billion in NDB loans were dollar denominated, even though these were mainly projects characterized by local-currency expenditures. There were minimal import requirements in loans for transportation (29 percent), energy (26 percent), water/sanitation/irrigation (22 percent), social infrastructure (15 percent), and cleaner production (8 percent).

The bigger dilemma, though, is whether the BRICS are reconstituting from their lowest point, a year ago, when Bolsonaro dragged the bloc down into ‘spalling’ territory, in the context of Putin’s indefensible invasion of Ukraine and ongoing Sino-Indian border conflicts. Here’s hype from Baroud:

As BRICS strengthens, it will have the potential to help poorer countries without pushing a self-serving political agenda, or indirectly manipulating and controlling local economies. As inflation is hitting many western countries, resulting in slower economic growth and causing social unrest, nations in the Global South are using this as an opportunity to develop their own economic alternative. This means that groups like BRICS will cease being exclusively economic institutions. The struggle is now very political…The BRICS countries, in particular, are leading the charge and are set to serve as the facilitator of rearranging the world’s economic and financial map.

This is Richard Wolff’s question:

Will some multinational new world order emerge and shape a new world economy? The most interesting possibility and perhaps the likeliest is that China and the entire BRICS (Brazil, Russia, India, China, and South Africa) grouping of nations will undertake the construction and maintenance of a new world economy. The war in Ukraine has already enhanced the prospects of such an outcome by strengthening the BRICS alliance. Many other countries have applied or will soon apply for entry into the BRICS framework. Together, they have the population, resources, productive capacity, connections, and accumulated solidarity to be a new pole for world economic development. Were they to play that role, the remaining parts of the world from Australia and New Zealand to Africa, Europe, and South America would have to rethink their foreign economic and political policies. Their economic futures depend in part on how they navigate the contest between old and new world economic organizations.

The problem, as I just witnessed last week at the IMF/World Bank protests, is that the new BRICS are still tied into the “old world” mode of neoliberal corporate multilateralism. The failure by Russia to go through with its recent threat to offer an alternative as Bank President to Ajay Banga – Washington’s predator choice to replace the climate-denialist Trump appointee David Malpass – is just one indicator. Nor have the BRICS made any obvious attempt to change IMF/Bank lending policies or ideology. The BRICS Bank’s and Asian Infrastructural Investment Bank joining financial sanctions against Putin is another indicator of financial-imperial stickiness.

The one anti-imperialist move by a BRICS leader against finance, was Putin’s default on international debt last year, but he really did want to pay back those loans, but was – he claimed – prevented from doing so by western financial sanctions. The only other defaults on foreign debt by BRICS countries were by Boris Yeltsin in 1998, by Brazil’s Jose Sarney in 1987 and by SA’s PW Botha in 1985 – but in each case it was due to lack of immediate hard currency.

Back in 2016, here’s the way it looked when I wrote up these same points for Third World Network:

BRICS finance ministers regularly expressed dissatisfaction with the International Monetary Fund’s (IMF’s) governance, notwithstanding having collectively spent $75 billion on the IMF’s recapitalization in 2012. To the surprise and disappointment of many BRICS supporters, however, the CRA actually empowers the IMF because, if a member country is in need of more than 30 percent of its borrowing quota it must first go to the IMF for a structural adjustment loan and conditionality before accessing more from the CRA. For South Africa, whose foreign debt rose from around $30 billion in 2003 to $150 billion a dozen years later – i.e., more than 40 percent of GDP, which puts it in the debt-crisis danger zone – this would mean that only $3 billion is available from the CRA before recourse to the IMF would be necessary. (In 1985, the last time this debt ratio was hit, the then leader of apartheid South Africa found it necessary to default on $13 billion in short-term debt payments coming due, to close the stock exchange and to impose exchange controls.)

Moreover, both the CRA and NDB are US dollar-denominated lenders, instead of establishing a fusion mechanism for their own monies: the real, ruble, rupee, renmimbi and rand. Such BRICS subservience would, remarked financier Ousmène Jacques Mandeng of Pramerica Investment Management in a Financial Times blog, ‘help overcome the main constraints of the global financial architecture. It may well be the piece missing to promote actual financial globalisation.’[1] As Brazil’s Ministry of Finance reminded in July 2015, the CRA ‘will contribute to promoting international financial stability, as it will complement the current global network of financial protection. It will also reinforce the world’s economic and financial agents’ trust.’[2]

Nevertheless, a great deal of the BRICS bloc’s credibility amongst progressive international political commentators rests upon aggressive rhetoric about potential global financial interventions. According to Horace Campbell, ‘Ultimately, in the context of the present currency wars, the CRA will replace the IMF as the provider of resources for BRICS members and other poor societies when there are balance of payments difficulties.’[3] Mark Weisbrot argued that the CRA ‘has the potential to break the pattern not only of US-EU global dominance but also of the harmful conditions typically attached to balance of payments support.’[4] According to Walden Bello, both the CRA and NDB ‘aim to break the global North’s chokehold on finance and development.’[5] Radhika Desai argues, ‘The BRICS are building a challenge to western economic supremacy.’[6] And after the Ufa summit, according to Mike Whitney of CounterPunch, ‘The dollar is toast. The IMF is toast. The US debt market (US Treasuries) is toast… Ufa marks a fundamental change in thinking, a fundamental change in approach, and a fundamental change in strategic orientation.’[7]

This wishful thinking is unfortunate not only because of the CRA’s provision that once the 30 percent quota on lending is breached an IMF agreement is required, thus providing a means of empowering and relegitimizing the IMF. Moreover, only CRA members (not other countries) get CRA access. Hence applause for the supposedly ‘alternative’ BRICS financial initiatives came logically from both Jim Yong Kim at the World Bank and Christine Lagarde at the International Monetary Fund. Likewise in 2015 more than 40 countries – including several from Europe including Britain – became founder-members of China’s Asian Infrastructure Investment Bank, and it received endorsement from Kim, in the process foiling Barack Obama’s sabotage diplomacy.[8]

In these respects, following Marini, the BRICS are ‘collaborating actively with imperialist expansion, assuming in this expansion the position of a key’ bloc, whose own interests also rest in sub-imperialist stabilization of international financial power relations, for the advancement of their own regional domination strategies. If this was not the case, it would have been logical for the BRICS to instead have supported the Banco del Sur (Bank of the South). Founded by the late Venezuelan president Hugo Chavez in 2007 and supported by Argentina, Bolivia, Brazil, Ecuador, Paraguay, and Uruguay, Banco del Sur already had $7 billion in capital by 2013.[9] It offered a more profound development finance challenge to the Washington Consensus, especially after Ecuadoran radical economists led by Pedro Paez improved the design. Instead, it was repeatedly sabotaged by more conservative Brazilian bureaucrats and likewise opposed by Pretoria, which refused to join it during the Mbeki era.

Read Ben Norton’s article on BRICS de-dollarization:

CGTN Interview with the new president of New Development Bank Dilma Rousseff

Transcript by CGTN

China and Brazil are members of the BRICS group, which established the New Development Bank in 2015 to fund development projects in emerging markets and developing countries. Now a former Brazilian president has become the new head of the multilateral bank. Wu Lei sat down with Dilma Rousseff to discuss her priorities during her term in office.

WU LEI CGTN Reporter: “As former president of Brazil, and economist who has been active in global development for a long time, what will be your priorities in terms of the NDB’s development in the coming years?”

DILMA ROUSSEFF President, New Development Bank: “It is very important to me that the New Development Bank, the bank of the BRICS, acts as a tool to support the development priorities of the BRICS and other developing countries.

We need to invest in projects that contribute to three fundamental areas. First, we need to support the countries with regards to climate change and Sustainable Development Goals. Second, we should promote social inclusion at every opportunity we have. And I believe we should finance their most critical and strategic infrastructure projects, and digital ones.

That said, we want to promote quality development.

Developing countries still don’t have the necessary infrastructure. They don’t have enough ports, airports and highways to meet their needs. And, many times, the ones they have are not adequate. They still have to build alternative and more modern models of transportation, for instance. I see China a country that has developed capability for alternative transportation at the scale and quality it needs. NDB has to support the other countries to also build their quality infrastructure as well, like high speed trains.

It is also very important to invest in technology and innovation. Invest in universities, for example. Our countries will not overcome extreme poverty if we don’t invest in education, science and technology.”

WU LEI CGTN Reporter: “What are some of the challenges the NDB faces now, given the current global situation? What role does the BRICS cooperation mechanism play?”

DILMA ROUSSEFF President, New Development Bank: “The world now is under the threat of high inflation and restrictive monetary policy, particularly in developed countries. Such monetary policy means a higher interest rate and, therefore, a higher probability of a reduction in growth and a higher probability of recession.

This presents an important question for the BRICS. We need a mechanism, a so-called anti-crisis mechanism, which must be countercyclical and support stabilization.

At the same time, it is necessary to find ways to avoid foreign exchange risk and other issues such as being dependent on a single currency such as the US dollar. The good news is that we are seeing many countries choosing to trade using their own currencies. China and Brazil, for instance, are agreeing to exchange with RMB and the Brazilian Real.

At the NDB, we have committed to it in our strategy. For the period from 2022 to 2026, NDB has to lend 30 percent in local currency, and so 30% of our loan book will be financed in the currencies of our member countries. That will be extremely important to help our countries avoid exchange rate risks and shortage in finance that hinder long term investments.”

*

Note to readers: Please click the share button above. Follow us on Instagram and Twitter and subscribe to our Telegram Channel. Feel free to repost and share widely Global Research articles.

Patrick Bond, Professor, University of the Western Cape School of Government. He is a regular contributor to Global Research.

Disclaimer: The contents of this article are of sole responsibility of the author(s). The Centre for Research on Globalization will not be responsible for any inaccurate or incorrect statement in this article. The Centre of Research on Globalization grants permission to cross-post Global Research articles on community internet sites as long the source and copyright are acknowledged together with a hyperlink to the original Global Research article. For publication of Global Research articles in print or other forms including commercial internet sites, contact: [email protected]

www.globalresearch.ca contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to our readers under the provisions of "fair use" in an effort to advance a better understanding of political, economic and social issues. The material on this site is distributed without profit to those who have expressed a prior interest in receiving it for research and educational purposes. If you wish to use copyrighted material for purposes other than "fair use" you must request permission from the

copyright owner.