Special Report by Outsiderclub.com

You might’ve seen graphene in the news lately because of the incredible advances it’s bringing about in the medical field, the energy sector, defense, and so on.

And here’s why: It’s 200 times stronger than steel, thinner than a sheet of paper, and more conductive than copper.

Researchers at the UK’s University of Manchester note it’s “almost one million times thinner than a human hair.”

“It is not only the thinnest material in the world,” says the New York Times, “but also the strongest: a sheet of it stretched over a coffee cup could support the weight of a truck bearing down on a pencil point.”

Bloomberg adds: “Lighter than a feather, stronger than steel, a superior electrical conductor to copper: According to its champions, graphene could unlock a new era of super energy-efficient gadgets, cheap quick-charge batteries, wafer-thin flexible touchscreen computing, and a sturdier light-weight automobile chassis.”

Bottom line: Graphene has the potential to completely revolutionize entire industries, creating bendable phones and touch screens… tiny self-powered oil and gas sensors… even synthetic blood that can be used in any person on the planet.

Incredible, isn’t it?

And because of its possible future applications in technology, it has been generating significant buzz among scientists worldwide since its discovery.

Strategic metal experts are already calling graphene the “… most important substance created since synthetic plastic a century ago!”

It’s no wonder the two Russian scientists who discovered it were awarded the Nobel Prize in physics — as well as knighthoods.

“Graphene doesn’t just have one application,” says Andre Geim, the Russian scientist who made the find along with Konstantin Novoselov.

“It is not even one material. It is a huge range of materials. A good comparison would be to how plastics are used.”

I’d say plastics is a conservative comparison. Graphene has far more high-tech uses than plastic — and is poised to be much more lucrative…

Scientists are hailing it as a miracle cure for industries ranging from fiber optic data transmission to nuclear energy to lithium-ion batteries.

Since graphene has a high strength-to-weight ratio, it’s the perfect material for use in automobiles, rockets, boats, turbine blades, airplanes, and more.

Take a look at what hundreds of researchers, companies, and governments are already doing with the strongest, thinnest, most conductive material ever discovered…

Engineers at Northwestern University have a made a graphene electrode that allows lithium-ion batteries to store 10 times as much power and charge 10 times faster.

MIT Engineering Professor Jeffrey Grossman believes solar cells made from graphene could produce 10,000 times more energy from a given amount of carbon than fossil fuels.

University of Manchester researchers have created a device that “could help detect the presence of drugs or toxins in the body or dramatically improve airport security.”

According to the Daily Mail: “A graphene credit card could store as much information as today’s computers,” and that “will lead to gadgets that make the iPhone and Kindle seem like toys from the age of steam trains.”

The BBC says: “It could spell the end for silicon and change the future of computers and other devices forever.”

Amazingly, the Israeli Army is even using the material to make invisible missiles.

Fact is graphene makes:

Solar – 50x-100x more efficient

- Semiconductors – 50x-100x faster

- Aircraft – 70% lighter

The applications for this “wonder material” appear endless.

This Super Material “Will Change the World.” — Huffington Post

I’m extremely bullish on graphene’s future prospects, and so is one of the men who discovered it, Nobel recipient Konstantin Novoselov:

“I don’t think it has been over-hyped… It has attracted a lot of attention because it is so simple — it is the thinnest possible matter — and yet it has so many unique properties. There are hundreds of properties which are unique or superior to other materials. Because it is only one atom thick it is quite transparent — not many materials that can conduct electricity are transparent.”

And speaking of transparent, scientists at the University of Texas, Dallas have made a graphene invisibility cloak by heating up a sheet of the material with electrical stimulation.

Again, this isn’t science fiction. This is happening right now.

Novoselov says, “It’s a big claim, but it’s not bold. That’s exactly why there are so many researchers working on it.”

So many, indeed: Over 200 companies are pursuing graphene opportunities, and it’s been the subject of thousands of peer-reviewed research papers.

Just recently, Bloomberg reported: “University-led research projects to investigate graphene won $1.35 billion in European Union funding.”

That’s a true testament of faith in this “wonder material.”

“Analysts say the first graphene-intensive products should come to market within 18 months,” says Businessweek, “with IBM, Samsung, and Nokia among those racing to be first.”

And now the global race is on — with a huge increase in patents filed to claim rights over different aspects of graphene…

The BBC reports: “A surge in research into the novel material graphene reveals an intensifying global contest to lead a potential industrial revolution.”

Graphite’s “Rare Earth” Situation

Yet only a few companies around the world have access to mineral graphite, which is the resource required to make graphene…

And up to this point, China has had a tight grip on the worldwide graphite supply, controlling over 70% of it.

Like it did with rare earths, China is limiting graphite exports with quotas — imposing a 20% export tariff and a 17% value added tax (VAT), causing graphite prices to rise. What’s more, due to environmental concerns, China has just ordered restrictions on any further graphite mines in two of its largest graphite producing regions.

All this has set the stage for non-Chinese based production of graphite to explode in a big way…

Leaving the door wide open for graphite mining operations in other parts of the globe — like our massive Alaskan discovery — as most of the world’s major economies perceive the mineral as being necessary for technological and industrial progression.

“China has a stranglehold on natural graphite supply,” says Simon Moores of Industrial Minerals. “This, together with a generation of under-investment in mines around the world, is creating a very tight supply situation.”

Already, Future Markets, Inc. reports a 4,000% increase in demand for graphene-based materials…

Which could send graphite prices soaring as demand for this mineral starts outpacing supply next year.

That’s why graphite has been named a “supply critical mineral” and a “strategic mineral” by the United States and the European Union.

Starting next year, the world will demand more graphite than is available…

And the supply/demand imbalance will only be worsened as these new sources of demand from graphene applications come online.

It’s no wonder prices have more than doubled since 2006, from $700 to $1,500 per tonne.

And that’s where our play on Northern Graphite Corp. (TSX-V: NGC) or (PK: NGPHF) comes in… We’re buying it below $1.00.

Background

We’ve all seen what the commodity supercycle has done to copper, gold, and many other resources.

Copper traded between $0.50 and $1.00 per pound for decades. And then, because of the commodity supercycle, it went over $4.00.

Same with gold. It used to sell for between $250 and $500 per ounce. Now it’s $1,600 per ounce.

That isn’t inflation. That’s the commodity supercycle.

Many things have caused this change, the big one being China, with India soon to follow.

And in the mining industry, the deposits we’ve lived off for years have been the big, low-cost, easy-to-find mines. Just like with oil.

But those mines are all getting deeper and older, so costs are increasing. Engineering and environmental standards have gone up and there’s been capital and cost inflation.

So gold can’t go back to $400 per ounce. And copper can’t go back to $1.00 per pound.

Graphite has been one of the last minerals to respond to this commodity supercycle. And the reason for that is there was excess production capacity from China. From 1990 until 2005, prices were in the tank.

Then, gradually, the growth in automobile and steel demand began to eat up that spare capacity and prices began to rise, and they steadily grew through 2008. But valuations of companies and deposits were slow to catch up.

When Northern Graphite got going in 2008, it only had a market cap of $2 million. Today, it’s valued around $50 million, but that’s still tiny compared to the +$1 billion resource it has in the ground.

CEO Greg Bowes was smart enough to see the commodity supercycle was slowly taking hold in the graphite industry. He knew the same thing that’s happened to copper, nickel, gold, wheat, and corn… would soon happen to graphite.

And it wasn’t on anyone’s radar yet.

He was correct. And graphite is starting to take off globally as the new hot commodity.

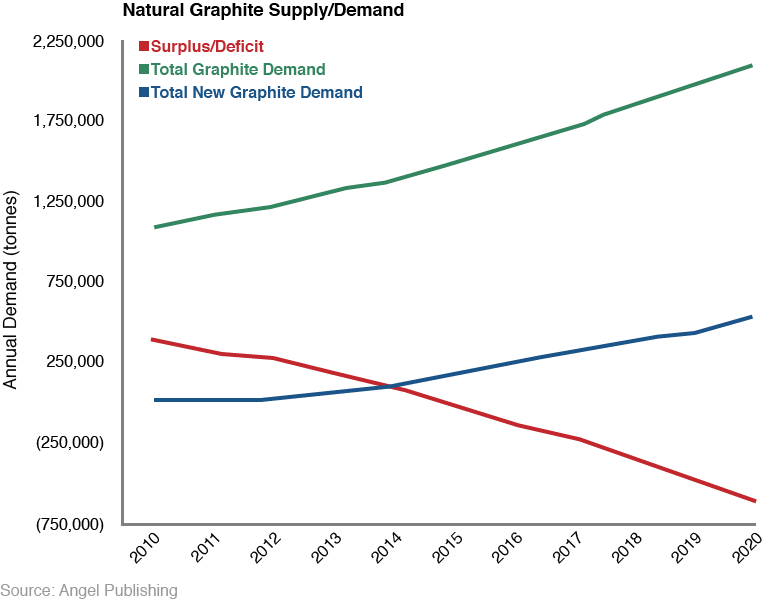

Graphite Prices

The price of graphite is up sharply in recent years thanks to a number of factors.

For starters, graphite is kind of in a “rare earth” type situation because 70% of supply is controlled by China. Industrialization in that country, as well as in India and other emerging markets, have led to increased demand for graphite in its traditional use as an additive to steel.

The 30% of supply that comes from outside of China is typically used in full by the country where it’s mined. There are only three graphite mines in North America.

So take a look at what all those various market factors have done to graphite prices in the last five years:

Why Northern Graphite?

Northern Graphite’s Bissett Creek mine is the closest to production of any public North American company. There is a 98 million tonne resource with 1.69 million tonnes of indicated graphite.

Graphite is different than copper or gold – where my copper is the same as your copper or your gold is the same as my gold.

With industrial minerals you have to look also at the physical and chemical properties of the product.

With graphite, the two main things to look for are flake size and carbon content. For flake size, larger is better, and you get a higher price for it. Graphite is pure carbon – the more impurities, the lower the price.

For example: If you produce a large flake concentrate that’s 90% carbon, you’re going to get, for example $1,400/tonne.

If you produce a large flake concentrate that’s 95% carbon – which doesn’t sound like a big difference – you’ll get double the price, about $2,800. You can see the large flake Northern Graphite has in this picture I took when I toured the property:

So when you look at a graphite mine, the first thing everybody focuses on right away is grade. And if you look at Northern Graphite, its grade is between 2% and 2.5%. There are graphite deposits in the world that are 10% to 15% – a significantly higher grade – but you have to look at what the mix of flake size and carbon content is, and the products it can produce.

Generally, the amount of large flake remains fixed and small, and if you have a higher grade it tends to be smaller, finer, and less valuable graphite that makes up the larger percentage.

For example, Focus Metals, a competitor, has a mine with a grade of 15%, but only 20% of that is large flake, 20% is medium flake, and 60% is powder, which is a low-value product.

Northern Graphite has a grade between 2 and 2.5%, but it’s nearly 100% flake. And 80%-90% of that is large flake. And much of it is nearly 98% carbon. A January 2012 pilot plant study proved how much large flake is there and that it contained over 97% carbon. I held some flake in my hand while i was there:

So the grade is lower, but the final product is much more valuable. In fact, Northern’s flake is so large, there aren’t really existing prices for it. It’s assumed they’d be somewhere near $3,000/tonne.

Using the conservative 80% figure, the company is looking at a 1.35 million tonnes of large flake, high carbon graphite. (1.69 million tonnes x .80).

Multiply that by a conservative $2,500/tonne (prices are only expected to rise), and you get a $3.37 billion resource. There will be costs for sure, including permitting, building the mine, extraction, consulting, etc.

But when an $0.89 company with a $33.4 million market cap is sitting on a $3.37 billion resource, I think the stock implications are clear.

The Mine

For this section, I’d like to turn to the thorough analyses done by Union Securities, Byron Capital Markets, and Mackie Research Capital.

From Union: The Bissett Creek project is located 100km east of North Bay, Ontario, and is easily accessible by a 17km gravel road from the Trans-Canada highway. The project area currently consists of 18 mineral claims and one mining lease, covering a total of 2,990 hectares. Northern Graphite has 100% interest in the Bissett Creek property with royalties of $20.00/t of concentrate on net sales.

From Byron: The Bissett Creek deposit is just 70 km east of Mattawa, Ontario. It is accessible by 17 km of well-maintained logging roads to the site, and the road is an easy turn off from Highway 17. The deposit is close enough to towns that the company does not have to construct a camp for its workforce. A natural gas pipeline and electric power also run along Highway 17, which Northern Graphite can tap into to run its operations. The location is an enviable one, as the company is costing three power scenarios to determine the most economic: 1) connect to the nearby natural gas pipeline; 2) connect to the closest substation; or 3) construct a new substation closer to the property. Low capital costs due to the deposit’s proximity to infrastructure will shorten the payback for the company and enhance shareholder value.

The resource is sufficient for over 35 years of production at 20,000 tonnes per annum (tpa) using a 1.5% graphitic carbon cut-off grade. The deposit is associated with larger flake material with all material expected, after processing, to remain at greater than 100 mesh size while being over 94% carbon concentrate.

From Mackie: A total resource amounting to 14.7 million tonnes of indicated resources was identified and 18 million tonnes of inferred resources, at a cut-off of 1.5%. The technical report also concluded a base-case IRR of 24% at an extremely low, outdated price for large flake graphite of $1,700/tonne. Since publication of the technical report, comparable large flake prices have nearly doubled.

We calculate that these identified resources should be adequate to allow for a mine life of 20 years at an approximate graphite production rate of 40,000 tonnes per year. A PEA has been completed by SGS that contemplated an operation producing 20,000 tonnes of graphite per year for 20 years. However, NGC plans on doubling the production rate in the first few years of operating to produce at this 40,000 tonne per year rate.

The Plan

A pilot plant test has been done and the results are in. A report in January 2012 showed:

The pilot plant has confirmed the technical viability and operating performance of the Company’s process plant design for the production of high purity, large flake graphite. Furthermore, results indicate that 50% of the graphite concentrate produced will be jumbo size, +48 mesh flake with a very high carbon content averaging 97.7% graphitic carbon (“Cg”). This is an exceptional product that will attract a premium price. The pilot plant test was designed, built and operated by SGS Minerals Services (“SGS”) in Lakefield, Ontario.

According to CEO Greg Bowes, “The pilot plant results have confirmed that the Bissett Creek deposit will produce entirely large flake, high carbon concentrates from flotation alone, without chemical or thermal treatment. As a result, we believe that Bissett Creek concentrates will have the highest average value per tonne in the industry and that this will also result in the highest margin in the industry. We will have the option of selling them into current high value markets, or using them to produce spherical graphite for Li ion batteries if it is financially advantageous to do so. Based on our review of publicly available information, it appears that over 50% of the production from most other graphite deposits will be very fine, -150 mesh lower carbon material, and it is generally not suitable for Li ion batteries or other high growth markets.”

A mine closure permit is expected in 2013, as well as an upgraded resource estimate that will make the project even more economic.

Production is expected in 2014.

Conclusion and Recommendation

From Mackie: We value Northern Graphite with a 12-month target price of $2.10 based on a 20-year DCF. Over 34 million indicated and inferred tonnes have been identified at the project to date. Based on our calculations, this is an adequate resource number for 20 years of production with a 2-year ramp-up period, whereby the peak production rate of approximately 5,000 tpd is achieved in 2016. A base-case 12% discount rate has been assumed to account for the pre-production, pre-bankable feasibility study stage of the project. As the project reaches milestones to bring it closer to production, it is likely that we would reduce the discount rate to account for decreased risk. NGC is currently conducting engineering and investigative work on the construction of a plant that would produce anode material for the lithium-ion battery market. The timeline for a construction decision is not expected until early in 2012, and although details on this prospect are scant, high-level cash-flow modeling indicates that this venture has the potential to deliver value many times over that of NGC’s current stock price. We do not currently include the Anode Plant in our valuation. However, we note that this project has the potential to increase our target price by approximately $1.00/share.

We view Northern Graphite Corporation as a very unique resource development opportunity within the Strategic Metals sector. We initiate coverage on Northern Graphite Corporation with a SPECULATIVE BUY recommendation and a 12- month target price of $2.10, based on our DCF calculation.

From Byron: We estimate that the capital costs to build the mine will be $70 million with half of the capital costs being financed with debt at 10% for a duration of 10 years with the remaining $35 million through raised equity. Production will begin in 2013 at a rate of 19,000 tpa of graphite, with 70% sold at +48 mesh size at an average price of $2,200/tonne while the -48+100 mesh size graphite would be the remaining 30% being sold at $1,800/tonne graphite. On the cost side, we have taken operating costs to approximately $1,100/tonne graphite produced. This takes into consideration the simple flow sheet of mine, crush, grind, float and re-float while achieving 95% yield, which is in- line with previous metallurgical work and should be confirmed again in September 2011. Additionally, we have taken into consideration the $20/tonne royalty on graphite produced. Given our expectation that graphite demand growth will continue, especially for larger flake graphite used in Li-ion batteries, and Northern Graphite’s ability to scale up the project, we expect the company to double production in 2016 to meet that surging demand, mainly from the automotive sector. We have used conservative pricing for Northern Graphite’s large flake 94% carbon content material. Thus, less conservative graphite pricing can dramatically increase the value of the project.

Northern Graphite is a late stage graphite mine developer that should have a producing mine by selling high-value graphite flakes in 2013 into the growing lithium-ion battery market. The company has begun the permitting process and given that the project flow sheet is simplistic and infrastructure is nearby, construction time should be about one year. We believe Bissett Creek’s deposit size will also allow for Northern Graphite to more than double its production while maintaining over 20 years of resource.

Graphite prices have exploded over the past year, as China dominates the market with over 70% of market share and imposing a 20% export duty and a 17% value added tax on its graphite. Northern Graphite’s ability to come to market quickly and cheaply will allow the company to take advantage of the situation as well as continue to deliver continued news flow to the investor.

With known metallurgy, infrastructure in place, a relatively low capex and a short time to production, risk is minimized for the Bissett Creek project that is expected to have $19.5 million per year in gross profit in 2013, with the potential to generate $39 million in gross profit by doubling production to meet demand from growing battery production. We are initiating coverage on Northern Graphite with a speculative buy rating and $1.90 target price based on 1.0x NAV using a 14% discount rate.

From Union: We have assumed that Northern Graphite will have the required permits in hand and begin construction in early 2012 with production commencement in Q1 2013. Similar to the current PEA, we have assumed the mill will have a nameplate capacity of 2,500tpd. Based on our start-up schedule and reserve assumptions, we have modeled a 30-year mine life for Bissett Creek. Given the higher grade of targeted initial pit upon commencement, the grade will be greater in the mine’s early years. However, at this time we have assumed that the head grade at Bissett Creek will be an average grade of 2.24% graphitic carbon throughout the project’s mine life.

We estimate that Northern Graphite’s NAV is $2.62 per share. We are initiating coverage on Northern Graphite Corp. with a $2.00 target price and a Strong Buy recommendation. Our target price is based on a 0.8x multiple of our Net Asset Value estimate for the company. Despite Northern Graphite’s strong management team, and positive fundamentals of the graphite market, we believe that the target multiple is justified given the stage of development of Bissett Creek. We believe that the Company has the required technical and managerial capacities to meet its permitting and construction goals, and will ultimately succeed in bringing Bissett Creek into production. As Northern Graphite demonstrates this in the short and medium term, this will be reflected in the target price going forward.

Outsider Club, Copyright © 2013, Angel Publishing LLC. All rights reserved.