The decision of Germany’s Bundesbank to repatriate part of its Gold Reserves held at the New York Federal Reserve bank has triggered a frenzy in the gold market.

German news sources suggest that a large portion of the German gold stored in the vaults of the New York Fed and the Banque de France is to be moved back to Germany.

According to analysts, this move could potentially “trigger a chain reaction, prompting other countries to start repatriating the gold stored in London, New York or Paris…. “

If gold repatriation becomes a worldwide trend, it will be obvious that both the US and UK have lost their credibility as gold custodians. For gold markets worldwide, this move may mark a switch from “financial gold” to “physical gold”, but the process is definitely in its early stages.

The decision to repatriate the German gold is a big victory for a part of the German press that first forced the Bundesbank to admit that 69% of its gold is stored outside Germany. Almost certainly both the German press and at least several German lawmakers will demand a verification procedure for the gold bars returned from New York, just to make sure that Germany doesn’t receive gold-plated tungsten instead of gold. It seems that German decision makers no longer trust their American partners. (Voice of Russia, January 15, 2013, emphasis added)

While the issue is actively debated in Germany, US financial reports have downplayed the significance of this historic decision, approved by the German government last September.

Meanwhile, a “Repatriate our Gold” campaign has been launched by several German economists, business executives and lawyers. The initiative does not apply solely to Germany. It calls upon countries to initiate the homeland repatriation of ALL gold holdings held in foreign central banks.

While national sovereignty and custody over Germany’s gold assets is part of the debate, several observers –including politicians– have begged the question: “can we trust the foreign central banks” (namely the US, Britain and France) which are holding Germany’s gold bars “in safe keeping”:

…Several German politicians have … voiced unease. Philipp Missfelder, a leading lawmaker from Chancellor Angela Merkel’s center-right party, has asked the Bundesbank for the right to view the gold bars in Paris and London, but the central bank has denied the request, citing the lack of visitor rooms in those facilities, German daily Bild reported.

Given the growing political unease about the issue and the pressure from auditors, the central bank decided last month [September] to repatriate some 50 tons of gold in each of the three coming years from New York to its headquarters in Frankfurt for ‘‘thorough examinations’’ regarding weight and quality, the report revealed.

…Several passages of the auditors’ report were blackened out in the copy shared with lawmakers, citing the Bundesbank’s concerns that they could compromise secrets involving the central banks storing the gold.

The report said that the gold pile in London has fallen ‘‘below 500 tons’’ due to recent sales and repatriations, but it did not specify how much gold was held in the U.S. and in France. German media have widely reported that some 1,500 tons — almost half of the total reserves — are stored in New York.

( Associated Press, Oct 22, 2012, emphasis added )

A full and complete repatriation of gold assets, however, is not envisaged:

“The Bundesbank plans to transfer 300 tonnes of gold from the Federal Reserve in New York and all of its gold stored at the Banque de France in Paris, 374 tonnes, to Frankfurt. beginning this year,

By 2020, it wants to hold half of the nearly 3,400 tonnes of gold valued at almost 138 billion euros – only the United States holds more – in Frankfurt, where it stores about a third of its reserves. The rest is kept at the Federal Reserve, the Banque de France and the Bank of England. (Reuters, January 16, 2012)

The German Federal Court of Auditors has called for an official inspection of German gold reserves stored at foreign central banks, “because they have never been fully checked“.

Are these German bullion reserves held at the Federal Reserve “separate” or are they part of the Federal Reserve’s fungible “big pot” of gold assets.

Does the New York Federal Reserve Bank have “Fungible Gold Assets to the Degree Claimed”? Could it reasonably meet a process of homeland repatriation of gold assets initiated by several countries simultaneously?

According to the NY Federal Reserve, 98% of its gold bullion reserves is in custody, i.e. it belongs to foreign countries. The remaining 2% belongs to the IMF and the NY Federal Reserve Bank. In a bitter irony the actual gold reserves of the NY Federal Reserve Bank are minimal.

Why is German Gold held outside Germany?

“Why is our gold in Paris, London and New York” and not in Frankfurt ?

The official explanation –which borders on the absurd– is that West Germany at the outset of the Cold War decided to store its central bank gold assets in London, Paris, and New York to “put them out of reach of the Soviet empire” which was allegedly intent upon looting West Germany’s gold treasures.

According to Reuters:

As the Cold War set in, Germany kept its gold reserves put, keeping them out of reach of the Soviet empire. But government officials have grown uneasy about the storage set-up and have called for the Bundesbank to inspect the bars.

The Bundesbank now wants to change the arrangement too, even though it has said it does not see a need to count the bars or check their gold content itself and considers written assurances from the other central banks as sufficient.

With the end of the Cold War it was no longer necessary to keep Germany’s gold reserves “as far to the west and as far from the Iron Curtain as possible”, Bundesbank board member Carl-Ludwig Thiele told reporters on Wednesday.

The Bundesbank gained more space in its vaults after the transition to the euro from the deutschmark. Reuters, January 16, 2013)

According to the Western media, in chorus, the threats of the “evil empire” in the course of the Cold War era had so to speak encouraged the “looking after” and “safe-keeping” of billions of dollars of German gold bullion in the secure central bank vaults of France, England and America. This was a “responsible” initiative undertaken by these three countries –“friends of West Germany”– with a view to allegedly assisting the Bundesbank located in Frankfurt am Main against an imminent attack by The Red Army.

But now more than 21 years after the official end of the Cold War (1991), the Bundesbank “plans to bring home some of its gold reserves stored in the United States’ and French central banks, bowing to government pressure to unwind a Cold War-era ploy that secured the national treasure.”

What was the objective of the US, in the wake of the World War II in pressuring countries to deposit their gold bullion in the custody of the US Federal Reserve?

Historically, the accumulation of gold bullion in the vaults of the US Federal Reserve (on behalf of foreign countries) has indelibly served to strengthen the global dollar system, both during the period of the (Bretton Woods) post-war “gold exchange standard” (1946-1971) as well as in its aftermath (1971-).

History: In the Wake of World War II

The gold bullion storage arrangement has nothing to do with the Soviet threat, as conveyed in official statements.

It has a lot to do with the history of World War II and its immediate aftermath.

The early postwar central banking arrangement was dictated by the Victors of World War II, namely America, France and Britain.

The military occupation governments of these three countries directly controlled the post-war monetary reforms implemented in West Germany starting in 1945.

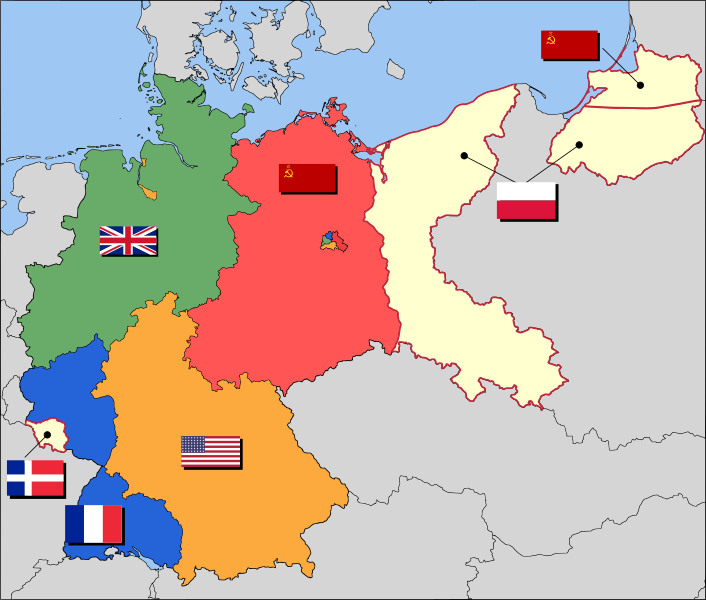

West Germany had been split up into three zones, respectively under the jurisdiction of the US, Britain and France (see map below). From 1945 to 1947, The Reichmark continued to circulate with new paper money printed in the US.

__________________________________________________________________________________________________________________________________

Post-Nazi German occupation borders and territories. Areas in beige indicate territories east of the Oder-Neisse line that were attached to Poland and the USSR. The Saar Protectorate, on the lefthand side of the map, is also shown in beige. Berlin is the multinational area shown within the red Soviet zone. (source: Wikipedia)

__________________________________________________________________________________________________________________________________

In 1947, the US and UK controlled occupation zones merged into an Anglo-American “BiZone”. In 1948, under a so-called “First Law on Currency Reform”, the occupation military government set up the Bank deutscher Länder (Bank of the German States) in liaison with the US Federal Reserve and the Bank of England. The currency reforms were implemented in parallel with the Marshall Plan, launched in June 1947.

The Bank deutscher Länder (BdL) was to manage the monetary system of the Länder (equivalent to states in a federal structure) in the Bizone under the jurisdiction of the US-UK military government, leading to the establishment of the Deutsche Mark in June 1948, which replaced the Reichsmark.

Ludwig Erhard –who became Finance Minister under the FGR government of Conrad Adenauer and then German Chancellor (1963-1966)– played a central role in the process of monetary reform. He started his political career as an economic consultant to the US military Government (USMG). In 1947, he was appointed chairman of the currency reform commission. From January 1947 to May 1949, the US military governor of the US zone (USMG) who supervised the setting up the new currency arrangement was General Lucius D. Clay, nicknamed “Der Kaiser”.

The Deutsche Mark initiative was then extended to the occupation zone controlled by France in November 1948 (“TriZone” arrangement), with the inclusion and participation of the Banque de France.

While the Federal Republic of Germany (FRG) (Bundesrepublik Deutschland), was created in May 1949, the Bundesbank only came into existence 8 years later, in 1957.

Germany’s gold reserves were under the jurisdiction of the Bank deutscher Länder (and subsequently of the Bundesbank). But the BdL was an initiative of the US-UK-France military occupation governments.

Of significance, under the Bretton Woods gold exchange standard (1946-1971), the dollar denominated export revenues accruing to West Germany were converted into gold at 32 dollars an ounce. In other words, the export earnings resulting from the sale of German commodities in the US market were, in a sense, “returned” to America in the form of gold bullion which was deposited for “safe-keeping” at the New York Federal Reserve Bank.

The important question is the following:

Did the procedures and agreements determined by the occupation military governments in 1947-48 envisage a framework whereby part of West Germany’s gold bullion was to be held in the victors’ central banks, namely the Bank of England, the US Federal Reserve and the Banque de France?

Gold Reserves from the Third Reich

The issue of the gold reserves of the Third Reich is a subject matter in itself, beyond the scope of this article.

A couple of observations: As of 1945, large amounts of gold from the Third Reich were transferred into custody of the military governments. Part of this gold was used to finance war reparations:

In September 1946, the United States, Britain, and France established the Tripartite Commission for the Restitution of Monetary Gold (TGC). The commission has its roots in Part III of the Paris Agreement on Reparation, signed on January 14, 1946 concerning German war reparations. Under the 1946 Paris Agreement, the three Allies were charged with recovering monetary gold looted by Nazi Germany from banks in occupied Europe and placing it in a “gold pool.”

Claims against the gold pool and subsequent redistribution of the gold to claimant countries were to be adjudicated and executed by the three Allies. ” ( for further details see US State Department, Tripartie Gold Commission, February 24, 1997,

A Foreign Exchange Depositary (FED) had been established at the Reichbank in Frankfurt. Referred to as “the Fort Knox of Germany”, a process of collection had been established `by the FED on behalf of the Allied Occupation Council.

Gold was collected by the FED, both in monetary and non-monetary form. By October 1947 –coinciding with the establishment of the Bank deutscher Laender– the FED, had accumulated 260 million dollars of monetary gold (at the 1947 price of gold, this represented a colossal amount of bullion).

A large part of this gold was restituted to different claimant countries, organizations and individuals. In 1950, the remaining assets of the FED –which were minimal, according to the US State Department– were transferred to the Bank deutscher Laender. (William Z. Slany, US Efforts to Restore Gold and Other Assets Stolen or Hidden by Germany During World War II, US State Department, Washington, 1997, p. 150-59).

Note:

Germany´s 3,400 tons of gold reserves does not pertain to gold from the pre-1945-era. Moreover, while the procedures of West Germany’s monetary reform under allied military occupation (1947-48) were instrumental in setting the foundations of German central banking in the post-war era, the initial amounts of gold bullion deposited in the early days of the Bank Deutscher Laender were minimal and of little significance.

It is understood that outside the realm of central banking and monetary reform, the allied forces of World War II including the US, Britain, France and the USSR did appropriate part of the gold of the Third Reich. This in itself is an entirely separate and complex issue which is beyond the scope of this article.